📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-06-25 09:51 JST)

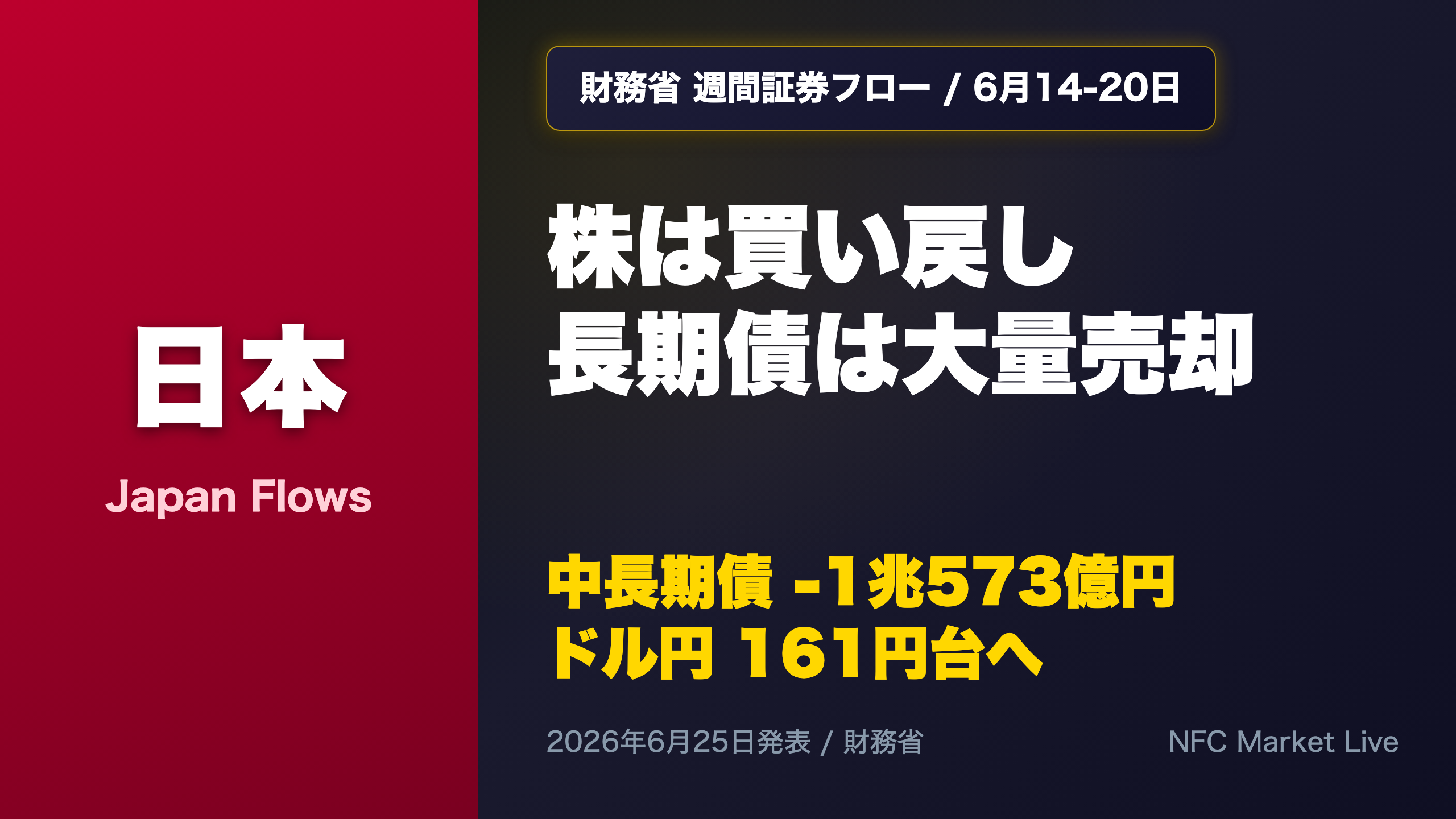

Deep dive into Japan’s weekly securities flows (Jun 14-20) released by the Ministry of Finance on Jun 25. Foreign investors bought 479.4bn yen of Japanese equities while dumping 1.057 trillion yen of long-term JGBs. We analyze this divergence against the backdrop of USDJPY breaking into the 161 range, with one year of historical context. Not investment advice.

総括:株は買い戻し、長期債は大量売却という二極化

Overview: Stocks and Long Bonds Split in the Same Week

Japan’s Ministry of Finance (MOF) publishes weekly data on cross-border securities transactions, one of the most-watched gauges of foreign and domestic capital flows. Unlike the US TIC data, which is monthly, this Japanese series is weekly, offering a high-frequency read on positioning.

The Numbers (in 100mn yen)

| Flow | Latest (Jun 14-20) | Prior (Jun 7-13) |

|---|---|---|

| Foreigners: Japan equities | +4,794 | -7,851 |

| Foreigners: long-term JGBs | -10,573 | -5,310 |

| Japanese: foreign equities | +4,268 | -4,183 |

| Japanese: foreign long bonds | +1,997 | +3,826 |

Foreign equity flows flipped to their first net buy in three weeks, while foreign selling of long-term JGBs nearly doubled versus the prior week, exceeding one trillion yen.

Bull vs Bear Reading

- Bull: Equities were bought back, and Japanese investors also bought both foreign stocks and bonds — risk appetite has partly recovered.

- Bear: The 1-trillion-yen outflow from long JGBs may reflect concern over Japanese duration/rate risk, especially with USDJPY at a yearly weak of 161.37.

Market Implication

For global investors, the divergence matters: JGB selling pressure can lift Japanese long-end yields, while the weak yen (161 vs the dollar) raises the stakes for any policy response. Still, this is single-week data — too early to declare a structural trend. The next release (early July) will show whether the buy-stocks, sell-bonds split persists.

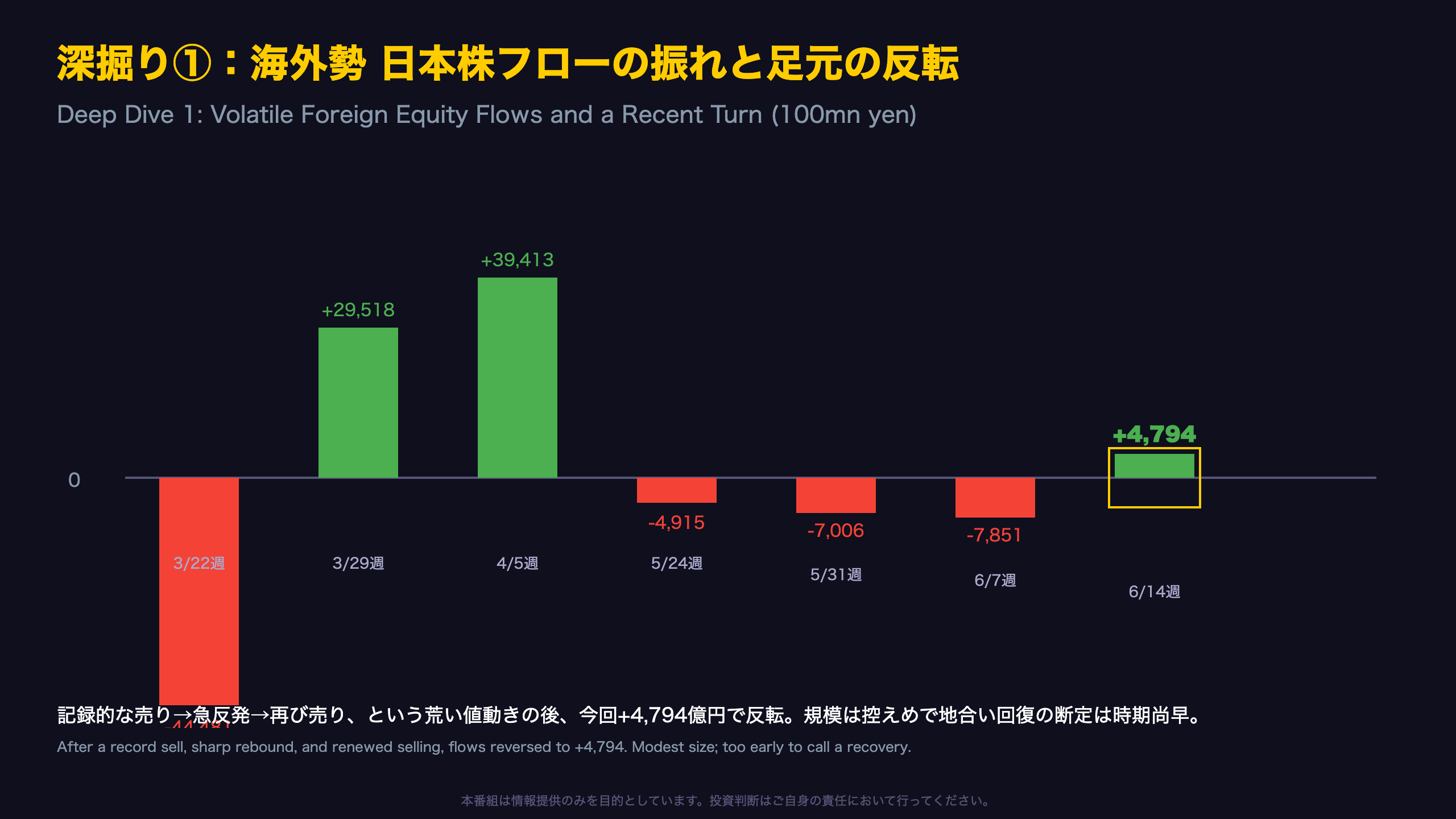

深掘り①:海外勢の日本株フローの振れと足元の買い戻し

Deep Dive 1: A Small Reversal Amid Violent Swings

Foreign flows into Japanese equities have been extraordinarily volatile in 2026. For overseas readers: this MOF series captures net purchases by non-residents, and it has whipsawed dramatically this year.

Key Turning Points (Foreigners, JP equities, 100mn yen)

| Week | Flow |

|---|---|

| Mar 22-28 | -44,481 (record sell) |

| Mar 29-Apr 4 | +29,518 |

| Apr 5-11 | +39,413 |

| May 31-Jun 6 | -7,006 |

| Jun 7-13 | -7,851 |

| Jun 14-20 | +4,794 |

After a record sell-off in late March and a V-shaped rebound in April, flows tilted back to selling from late May. This week marks a modest reversal, ending a three-week selling streak.

Two Readings

- Constructive: The sign flip may hint that selling pressure has run its course.

- Cautious: At +479bn yen, the magnitude is small versus April’s ~4-trillion-yen peak — too weak to confirm a sentiment recovery.

Notably, this buying occurred as USDJPY pushed into the 161 range. A weaker yen can make yen-denominated assets cheaper in foreign-currency terms, potentially supporting accumulation — though this is one plausible factor, not a confirmed cause. For global equity investors, watching whether the buy resumes next week is more informative than this single print.

深掘り②:中長期債からの1兆円超流出とデュレーション回避

Deep Dive 2: Foreign Bond Preference Splits by Maturity

The headline item is the 1.057-trillion-yen outflow from long-term JGBs by foreigners, nearly double the prior week’s 531bn, and among the largest in the past year.

Recent Long-Bond Flow Trend (Foreigners, 100mn yen)

| Week | Flow |

|---|---|

| May 24-30 | +12,502 |

| May 31-Jun 6 | -10,386 |

| Jun 7-13 | -5,310 |

| Jun 14-20 | -10,573 |

That is three consecutive weeks of selling since late May. Rather than a one-off, this may signal that foreign investors are increasingly avoiding Japanese duration risk — the risk of rising long-term yields.

A Maturity Split

Crucially, the contrast with short-term JGBs is sharp: foreigners bought 464bn yen of short bonds this week. So the pattern is “buy the short end, sell the long end” — a curve-aware selectivity consistent with hedging against higher long-end yields. For global rates investors, this resembles a duration-shortening posture seen when a central bank is expected to tighten or let the long end rise.

Caveat

Long-bond flows have flipped sign frequently over the past year (e.g., +1,883bn in the week of Feb 21). Three weeks of selling alone should not be declared a structural trend. The key watch item: whether the next release marks a fourth straight outflow.

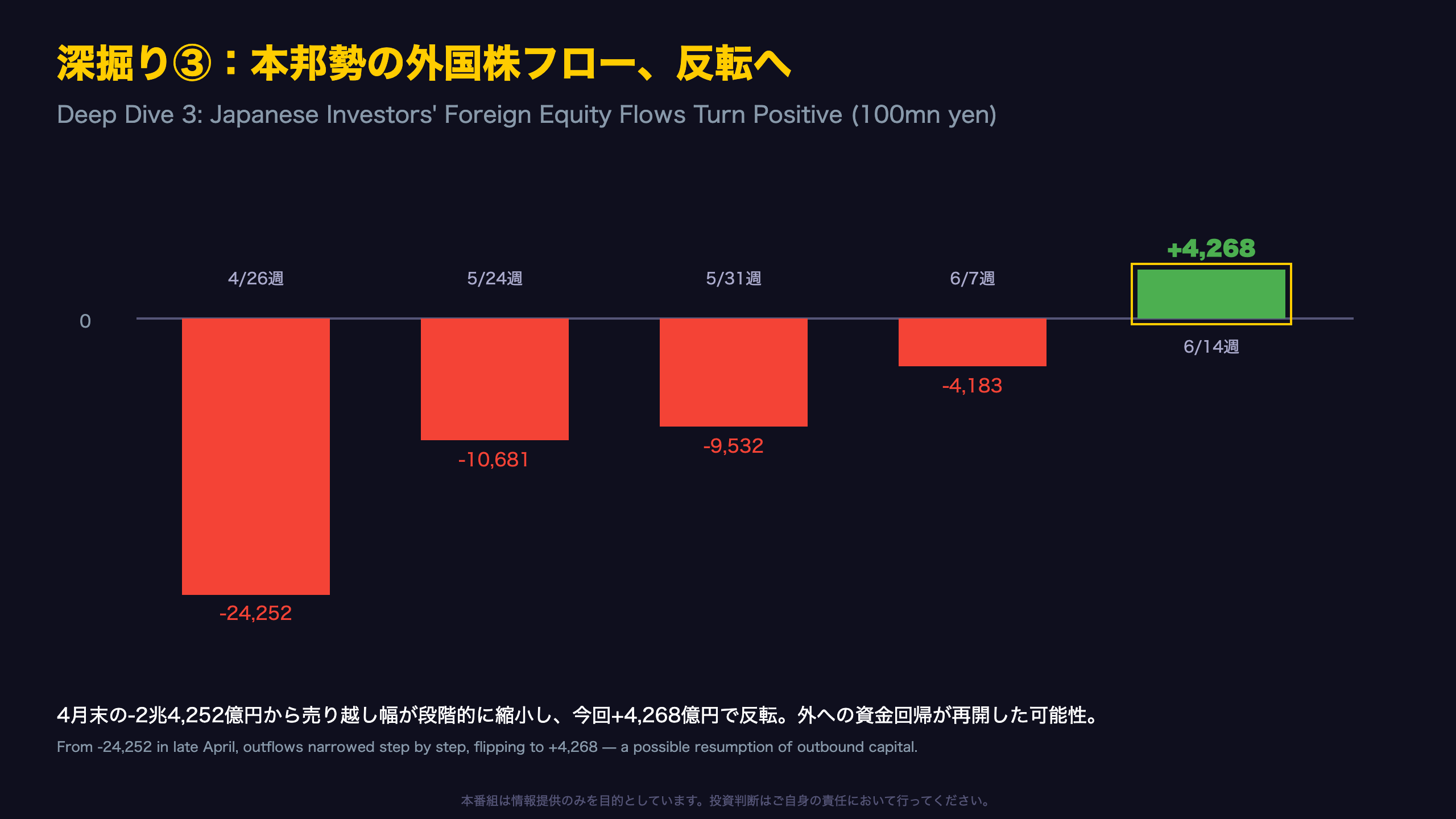

深掘り③:本邦勢の動向と「外への資金回帰」

Deep Dive 3: Japanese Investors Tilt Back Abroad

It is not only foreigners — domestic Japanese flows also reversed. This week, Japanese investors net-bought both foreign equities (+427bn yen) and foreign long-term bonds (+200bn yen).

Japanese Investors: Foreign Equity Flows (100mn yen)

| Week | Flow |

|---|---|

| Apr 26-May 2 | -24,252 |

| May 24-30 | -10,681 |

| May 31-Jun 6 | -9,532 |

| Jun 7-13 | -4,183 |

| Jun 14-20 | +4,268 |

After a heavy sell-off in late April, Japanese investors steadily reduced foreign equity holdings, but the outflows narrowed week by week before flipping positive — suggesting a possible resumption of capital flowing overseas.

Macro Implication

Japanese investors buying foreign bonds while foreigners sell long JGBs — a tug-of-war between yen and foreign-currency assets.

For FX-focused readers, these bidirectional flows create opposing pressures: Japanese buying of foreign assets is yen-negative, while foreigners selling JGBs and potentially repatriating could be yen-positive. The net effect on USDJPY depends on which side dominates.

Caveat

Yen weakness and the appeal of higher overseas yields are plausible drivers, but this is single-week data — not enough to declare a structural shift back to foreign assets.

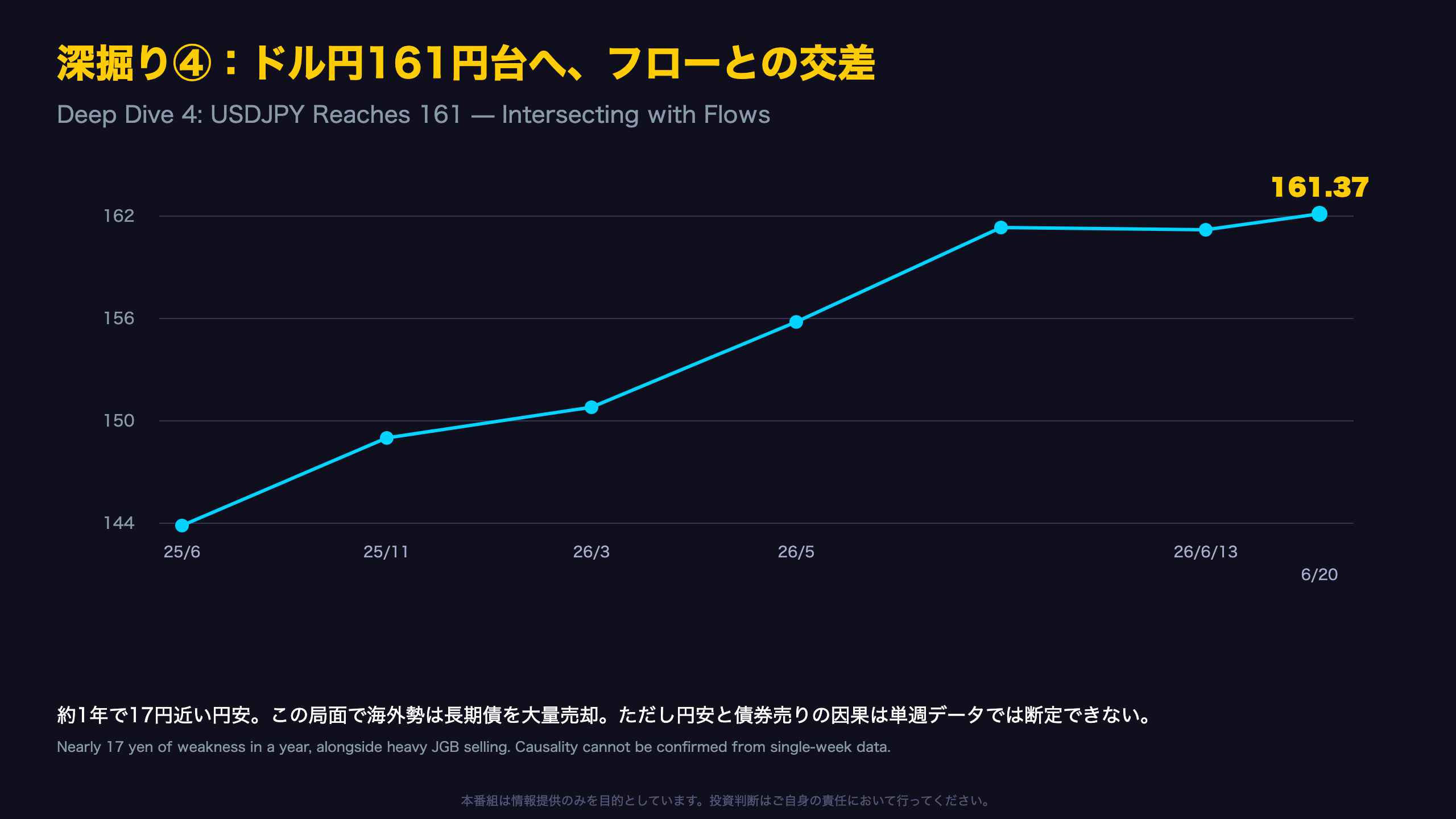

深掘り④:フローとドル円161円台の関係

Deep Dive 4: Where Yen Weakness Meets Flows

USDJPY hit 161.37 this week, the weakest yen reading in this dataset. The one-year path shows yen weakness is a persistent trend, not a blip.

USDJPY Milestones

| Week | USDJPY |

|---|---|

| Jun 28, 2025 | 144.74 |

| Nov 22, 2025 | 156.58 |

| Mar 28, 2026 | 160.16 |

| Jun 6, 2026 | 160.26 |

| Jun 20, 2026 | 161.37 |

That is nearly a 17-yen depreciation in about a year, with a fresh leg lower after consolidating in the 160s.

Chain of Reasoning

[Foreigners sold 1,057bn yen of long JGBs] → [In general, long-bond selling can reflect expectations of higher yen rates and rising hedging costs] → [Reduced appeal of yen assets can be one factor in yen-weakening pressure]

However, parts of this chain rely on general theory. This single week of data cannot establish causality between yen weakness and bond selling. Flows and FX moved together, so determining the leading factor requires caution.

For Global Investors

A yen near 161 raises the policy stakes: persistent weakness can pressure import costs and invite verbal or actual intervention. The interplay matters — Japanese investors buying foreign assets is yen-negative, while foreigners repatriating from JGB sales could be yen-positive. Watch whether 161 holds alongside next week’s flow data.

インプリケーション:市場への含意と注目点

Implications: Three Things to Watch

This week’s flows painted a complex picture mixing strength and weakness. Here is the chain-of-reasoning summary for global investors.

Chain: Rates

[Foreigners sold 1,057bn yen of long JGBs — 3 straight weeks] → [Generally reflects duration avoidance and higher rate expectations] → [Can be one factor pressuring Japanese long-term yields higher]

Note: the mechanism partly relies on general theory and cannot be confirmed from this data alone.

Chain: Risk Appetite

[Foreigners bought +479bn yen of equities; Japanese bought foreign assets] → [Two-way risk-taking coexists] → [Risk appetite appears partly intact]

Chain: FX

[Japanese buying foreign assets] → [Yen-selling demand] → [One factor in yen weakness] / while [foreigners selling JGBs] has ambiguous, two-way effects on yen supply-demand

Three Watch Items Next Release

- Bond flows: A fourth straight long-bond outflow would reinforce the duration-avoidance read.

- Equity flows: Was this week’s buying a one-off or the start of a trend?

- USDJPY: Does 161 hold, or does a correction set in?

For international investors, the configuration — buy stocks, sell long bonds, weakest yen — points to selective risk-taking alongside aversion to rate risk. With a yen near 161, intervention risk and BOJ policy expectations become central. Crucially, all of this is single-week data; confirming a trend requires the next prints.

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.