📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-07-12 08:38 JST)

This week’s global macro roundup (Jul 5-12).

📊 The Fed under new Chair Warsh scrapped its rate-cut bias entirely, with a unanimous 12-0 vote.

📈 The ECB also hiked rates unanimously after an April split decision.

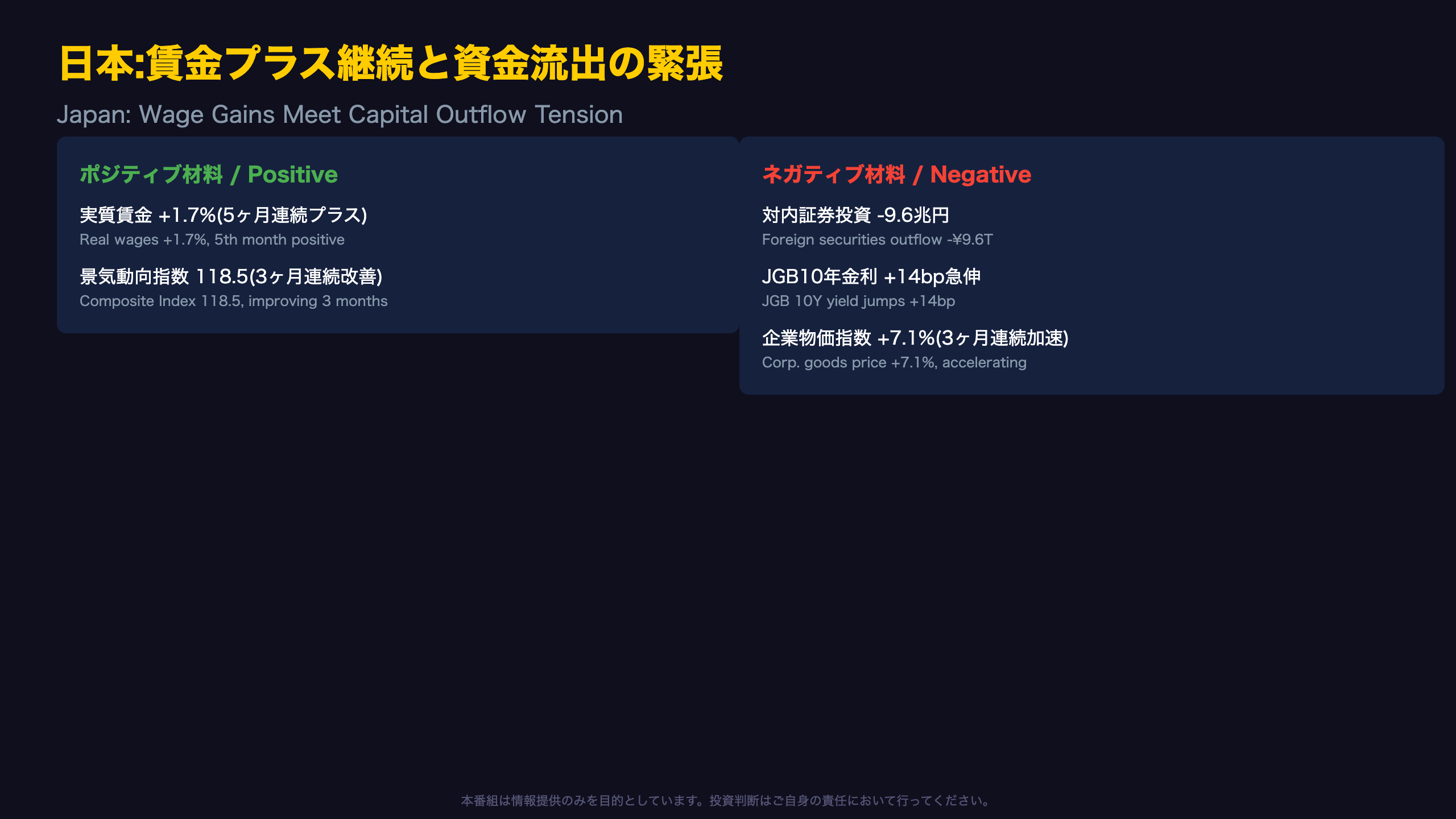

🇯🇵 Japan’s real wages rose for a 5th straight month, even as foreign investors pulled ¥9.6 trillion from Japanese securities and JGB yields jumped 14bp.

🇨🇦 Canada’s job growth slowed sharply, yet unemployment improved.

💡 Next week: watch US CPI, Brazil’s Focus survey, and Japan’s weekly capital flow data.

⚠️ Full analysis inside.

オープニング:今週のグローバルマクロ

This Week’s Highlights

The week of July 5-12, 2026 saw a cluster of major central bank communications hit the wires almost simultaneously. The Federal Reserve, under newly installed Chair Kevin Warsh, made a decisive hawkish turn, while the European Central Bank (ECB) — Europe’s counterpart to the Fed, setting monetary policy for the 20-nation eurozone — voted unanimously to hike rates. Mexico’s Banxico moved in the opposite direction, holding rates unanimously after previously leaning dovish.

Meanwhile in Japan, real wages extended a positive streak to five months even as foreign investors pulled a record ¥9.6 trillion (roughly $59 billion) from Japanese securities, and long-term JGB yields jumped sharply.

This deep dive walks through the data behind these headlines and what they mean for global asset allocation.

今週の総括:主要中銀、タカ派回帰の一週間

What the Regime-Diagnosis Signals Say

This week’s quant model flagged two ‘strong directional’ short signals (NZDMXN, NZDNOK) against two ‘weak’ long signals (USDMXN, EURNOK), a roughly balanced picture overall. Among the ten central bank models tracked, only Canada’s Bank of Canada (BOC) model reached ‘high confidence’ status (Mahalanobis distance 8.4, confidence 0.62), while the ECB model sat at medium confidence (0.24) and most others — including the Fed, BOJ, BOE, RBA, RBNZ, and Banxico — were flagged as ‘low confidence, far from centroid.’

As the report notes, “low-confidence models carry higher signal uncertainty” — a caveat worth keeping in mind before reading too much into any single directional call.

Bull vs Bear Read

The bullish interpretation: a synchronized hawkish shift across central banks reflects a shared, well-founded concern about inflation persistence. The bearish counter: Banxico’s dovish hold and the RBNZ’s softened forward guidance show that actions and words are diverging in several cases, making a blanket ‘global tightening’ narrative premature.

Looking Ahead

Next week’s data — particularly early-August US and Japan employment reports — will be the key test of whether this hawkish alignment holds or fragments.

米国ハイライト:FRBタカ派転換とインフレ加速

Treasury Auction Data Adds Another Layer

Alongside the Fed’s hawkish shift, Treasury auction data showed intriguing cracks in demand. The indirect bidder ratio (a proxy for foreign central bank and sovereign wealth fund demand) for the 13-week bill fell to 37.0% at the June 29 auction, down 17.8 points from June 22’s 54.8% — the weakest reading among the last 12 auctions. The bid-to-cover ratio also slipped from 2.68x to 2.32x.

However, the 26-week bill told the opposite story, improving from 48.7% to 62.1% over the same window, so a blanket claim of ‘foreign investors fleeing Treasuries’ would be premature. Notably, mid-term auctions (7-year, 5-year, 2-year notes) all posted indirect bidder ratios in the 47-53% range, actually lower than short bills (58-62%).

Wholesale Inventories: A Quiet Anomaly

The US Census Bureau’s Monthly Wholesale Trade Survey (an indicator watched for GDP inventory investment and inflation pass-through signals) showed inventory growth decelerating for a fourth straight month (from +0.9% in February to +0.1% in May) even as sales surged 18.1% year-over-year. The inventory-to-sales ratio, at 1.15, is near its tightest level since the pandemic supply-chain crunch.

The release explicitly states the 90% confidence interval “includes zero,” meaning May’s inventory change is not statistically distinguishable from no change at all.

What’s Next

The next FOMC meeting is July 28-29. Trade balance data drops August 4, and wholesale trade data follows August 6 — both key tests of whether this inflationary, tightening-friendly narrative holds.

日本ハイライト:実質賃金プラス継続の裏で進む緊張

Money Stock Data Reveals a Shift in “Quality”

The Bank of Japan’s money stock report for June showed M2 and M3 growth decelerating only slightly, but M1 (currency plus demand deposits, the most liquid tier) growth cratered from +0.3% to +0.1% year-on-year, turning negative (-1.0%) on a seasonally adjusted annualized basis. Meanwhile, time deposits (a less liquid tier) rose from ¥516.8T to ¥519.9T, suggesting money is moving from instantly-spendable cash into interest-bearing deposits — a pattern consistent with Japan’s ongoing exit from ultra-low rates.

Current Account vs FX Reserves: A Striking Divergence

The Ministry of Finance’s May balance of payments data showed the current account surplus widening to ¥3.97 trillion (+¥647.8B YoY), even as FX reserves fell by a striking ¥11.4 trillion. The source report gives no explanation; while large FX reserve drawdowns are often associated with currency intervention, this cannot be confirmed from this data alone — an important distinction for investors following USD/JPY.

Bull vs Bear

Bulls emphasize the durability of positive real wages and an improving Composite Index. Bears note that while 42.8% of June’s ¥9.6T outflow was in short-term bills (a more technical, less structural signal), the ¥5.5 trillion combined sell-off in stocks and long-term bonds alone is not trivial.

What’s Next

June real wage data is due August 5, and the Corporate Goods Price Index follows August 13 — both will clarify whether this week’s tension is transient or structural.

中央銀行マップ:タカ派化と据え置きの対比

The ECB’s “Not an Insurance Hike”

The ECB minutes explicitly state that June’s rate adjustment “should not be seen as an insurance hike but rather… robust across the baseline outlook and the full range of alternative scenarios.” The shift from April’s wait-and-see stance to June’s assessment that “the current situation no longer qualified as a case for looking through the shock” was driven by a reversal in core inflation (2.2% to 2.5%) and a jump in services inflation (3.0% to 3.5%).

RBNZ’s Action-Words Divergence

The Reserve Bank of New Zealand hiked 25bp (to 2.50%) unanimously, yet its risk assessment split 4-2 among committee members, and forward guidance language softened from “sooner and by more than envisaged” to “appear likely… timing is highly uncertain.” This is an unusual combination: hawkish in action, dovish in tone.

Banxico’s Full Dovish-to-Neutral Reversal

Mexico’s central bank moved from a narrow 3-2 rate cut in May to a unanimous 5-0 hold in June, with dovish-leaning members adopting arguments (“real ex-ante rates already near neutral”) previously voiced by dissenting hawks — better read as data-driven convergence than an ideological about-face.

What’s Next

The ECB’s July meeting minutes are due August 27. Specific dates for the next Banxico and RBNZ meetings were not disclosed in source material; the next regime-diagnosis update will be the key signal to watch for shifts in policy direction.

今週の番組制作費:AIによる自動化コスト

Cost Breakdown

The only disclosed cost data point this week comes from the July 7 trade balance episode: an LLM (Claude Sonnet 5) run using 49,367 input tokens and 65,632 output tokens, totaling ¥122 (converted at 1 USD = 162.1 JPY).

This figure covers LLM costs only — additional costs from text-to-speech synthesis, background music generation, and social media posting likely exist but were not itemized in this week’s data pack.

Economies of Scale

If the 18 episodes published this week were produced at a broadly similar cost, it would suggest AI-driven automation delivers substantial efficiency gains compared to traditional human-staffed research, scripting, and editing workflows. That said, this remains an inference from a single disclosed example, and per-episode token usage can vary meaningfully.

Multi-Format Distribution as Added Value

Simultaneously repackaging the same underlying analysis into video, X (Twitter), and blog formats is a distinguishing feature of an AI-driven pipeline — a volume of output that would be difficult for a traditional, human-staffed newsroom to match within the same week.

来週の注目イベント:7月13日〜17日

Brazil’s Focus Survey: A Chain of Evidence

Brazil’s year-end 2026 Selic forecast was hiked 50bp in just one month (from 13.50% to 14.00%), according to this week’s Focus Market Readout — the weekly survey of over 130 banks and asset managers that Brazil’s central bank, BCB (Banco Central do Brasil), itself uses as a policy input. If the 14.00% forecast holds steady next week, it would suggest inflation concerns are stabilizing; a further upward revision would instead reinforce expectations of a prolonged high-rate environment in Brazil.

Connecting to US CPI

This week’s FOMC minutes confirmed four consecutive months of accelerating core PCE inflation, from 2.8% in February to an estimated 4.1% in May. US CPI data, typically released mid-month (a general release-cycle expectation, not confirmed in this week’s source data), will be closely watched next week as a read on whether this inflationary trend is continuing ahead of the July 28-29 FOMC meeting.

Exact release dates were not specified in this week’s data pack; readers should confirm against official statistical agency calendars.

Will Japan’s Flow Pattern Repeat?

This week’s ¥9.6 trillion outflow from Japanese securities was concentrated in the back third of June (¥6.99T in the June 21-30 window alone, per MOF’s 10-day breakdown). Next week’s MOF weekly data will show whether similarly large swings recur around the month’s turn in July.

Bottom Line

Next week’s three watch points — Brazilian rate expectations, US inflation momentum, and the persistence of Japan’s capital outflows — will collectively test whether this week’s hawkish, outflow-driven narrative has staying power.

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.