📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-07-15 02:13 JST)

📄 Primary Source

NFC Market Live

https://www.youtube.com/live/ZO9HbvGe7cE

New Fed Chair Kevin Warsh delivered his first congressional testimony since taking office. 📊

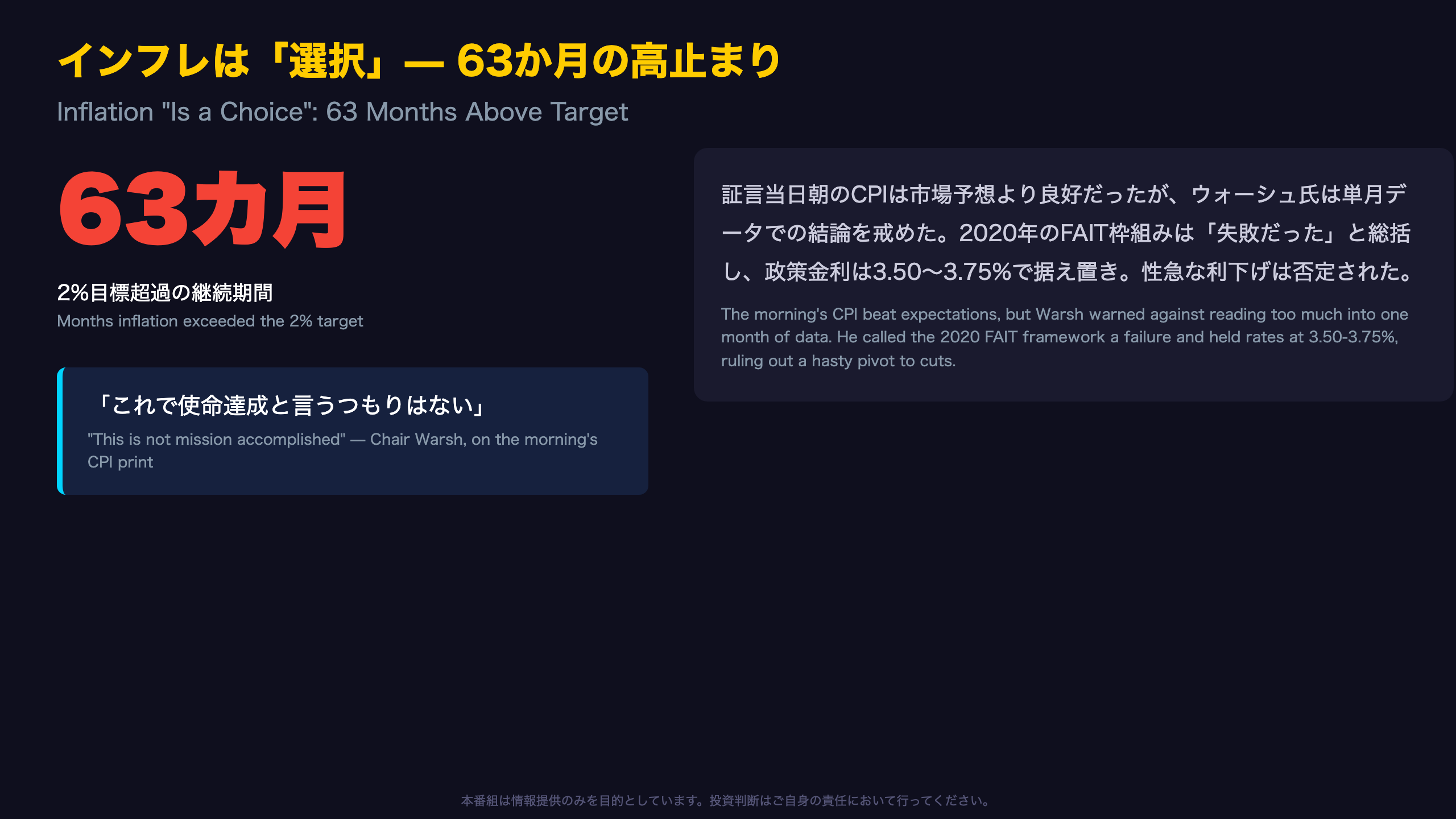

The FOMC held rates at 3.50-3.75%, while inflation has stayed above the 2% target for 63 straight months.

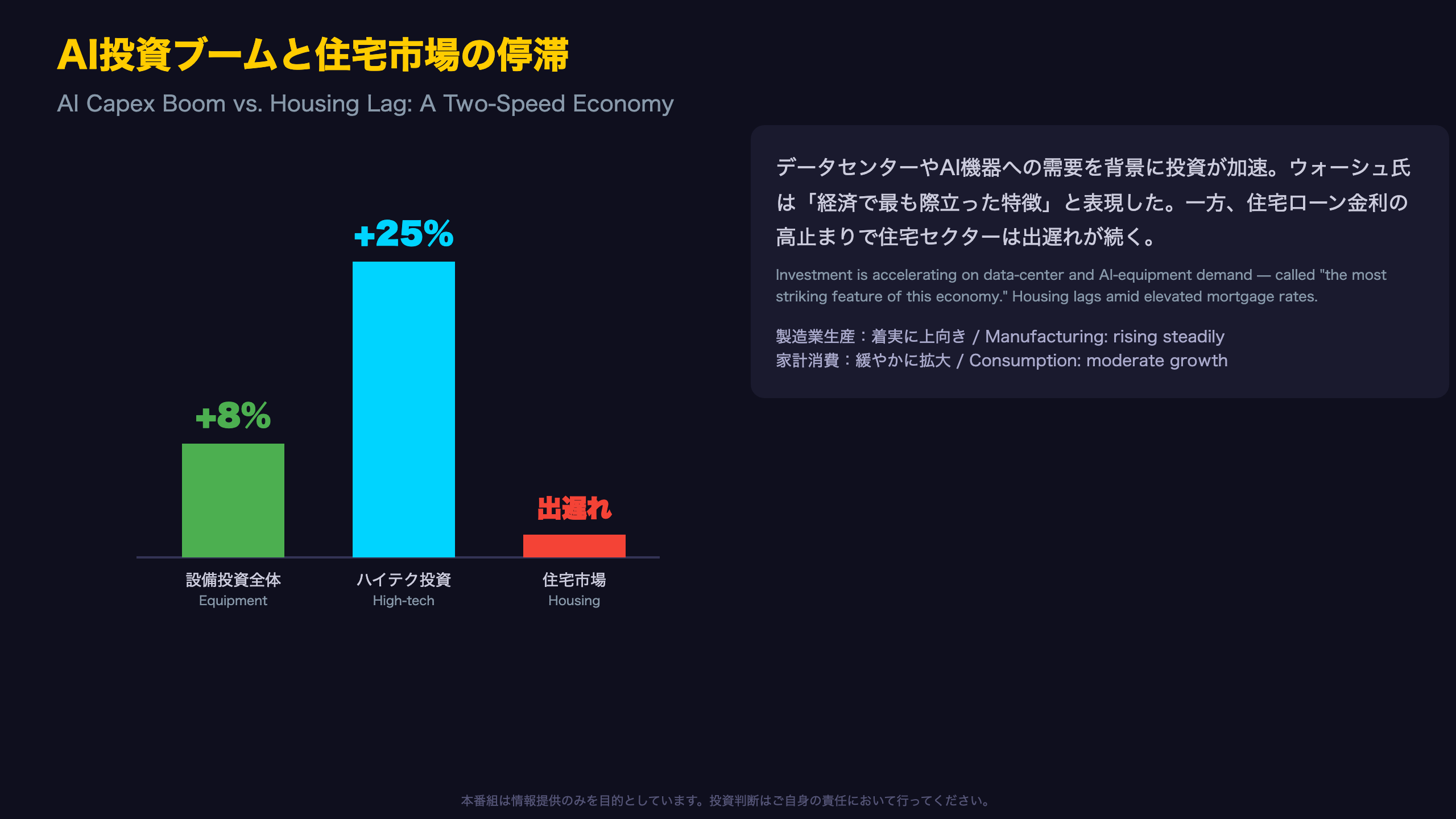

Yet equipment investment rose 8% YoY and AI-linked high-tech spending surged nearly 25%. 💡

Despite a better-than-expected CPI print on the morning of the hearing, Warsh refused to call it “mission accomplished” and outlined sweeping reforms to Fed communications and balance sheet policy. ⚠️

We break down the hawkish inflation stance alongside a genuinely two-speed U.S. economy. 📈

サマリー:二極化する経済とタカ派新議長

Season 1, Episode 1

Committee Chairman French Hill closed the hearing by joking that this was “Season 1, Episode 1” of Warsh’s tenure — a nod to the twice-yearly testimony cycle the Fed chair must now repeat. Warsh testified roughly seven weeks after his Senate confirmation hearing on April 21, 2026, an unusually fast turnaround for a new Fed chair’s first appearance.

Key numbers

- Policy rate: 3.50%-3.75% (held)

- Equipment investment (YoY): about +8%

- High-tech investment (YoY): about +25%

- Months inflation exceeded 2% target: 63

Warsh noted that \”underlying inflation over longer time horizons is determined largely by monetary policy,\” signaling he won’t overreact to single-month data swings.

Bull vs. bear read

Optimists see the AI capex acceleration and steady manufacturing output as the start of a new investment supercycle. Skeptics point to 63 months of above-target inflation and a housing sector that continues to lag as evidence of persistent strain on household purchasing power. Warsh himself explicitly rejected cherry-picking data to declare victory, positioning himself deliberately between these two camps.

What’s next

The next semi-annual testimony is typically in February. Five newly formed task forces covering communications, the balance sheet, data sources, productivity/jobs, and the inflation framework are expected to report conclusions by year-end.

インフレは「選択」— 63か月の高止まりと据え置き決定

Why He Won’t Call It “Mission Accomplished”

During testimony, Warsh explicitly stated that the morning’s CPI print was “positive relative to expectations,” but added, “I’m not for cherry-picking” a single data point to claim victory. This caution stems from the Fed’s own history of misjudging the 2021 inflation surge as merely “transitory.”

A 63-month timeline

Inflation has exceeded the Fed’s 2 percent target for 63 months — more than five years. Warsh described this as an “undue tax” that has burdened households and businesses for far too long, a phrase echoing themes raised by committee members as well.

Verdict on the 2020 framework

On the Fed’s August 2020 Flexible Average Inflation Targeting (FAIT) framework, Warsh said he was “very critical of it” even before joining the Fed, and stated plainly that “the framework did not succeed in its objectives.” He welcomed its abandonment in 2025 by his predecessors.

What to watch next

The next FOMC meeting is described as being “in a couple of weeks.” Whether the hold continues or shifts will likely hinge on early findings from the newly created inflation-framework task force, one of five groups Warsh has commissioned.

For international readers

Unlike the Fed’s dual mandate (price stability + maximum employment), many central banks such as the ECB or Bank of England operate with a single inflation mandate — a useful contrast when assessing how aggressively the Fed can lean into inflation-fighting relative to peers.

AI投資ブームと住宅市場の停滞 — 二速走行の実体経済

“AI Investment Will Soon Just Be Called Investment”

Warsh told lawmakers, “We don’t yet know fully the extent to which the economy will benefit from AI. Yet it seems inevitable that that which we’re now calling AI investment will soon just be called investment.” This suggests AI-related capex is becoming structurally embedded in the broader U.S. investment cycle rather than remaining a niche category.

The breakdown

- Overall equipment investment (YoY): about +8%

- High-tech investment (YoY): about +25%

- Manufacturing output: “moved up steadily” over the past year

- Household consumption: “moderate”

- Housing: “continues to lag”

Why housing lags

Warsh attributed elevated 30-year fixed mortgage rates “in part” to inflation running above the Fed’s target — implying that current policy restrictiveness is selectively weighing on rate-sensitive housing demand even as broader investment accelerates.

Bull vs. bear read

Optimists view the AI capex surge as a productivity catalyst likely to lift wages over time. Skeptics see the weak housing sector as a warning sign that rate-sensitive households are bearing a disproportionate burden, raising the risk of a widening gap between investment-led and consumer-led segments of the economy.

International context

For comparison, business investment cycles of this magnitude echo the late-1990s U.S. tech capex boom that Alan Greenspan (whom Warsh honored in his opening remarks) navigated at the Fed — a historical parallel investors may find instructive.

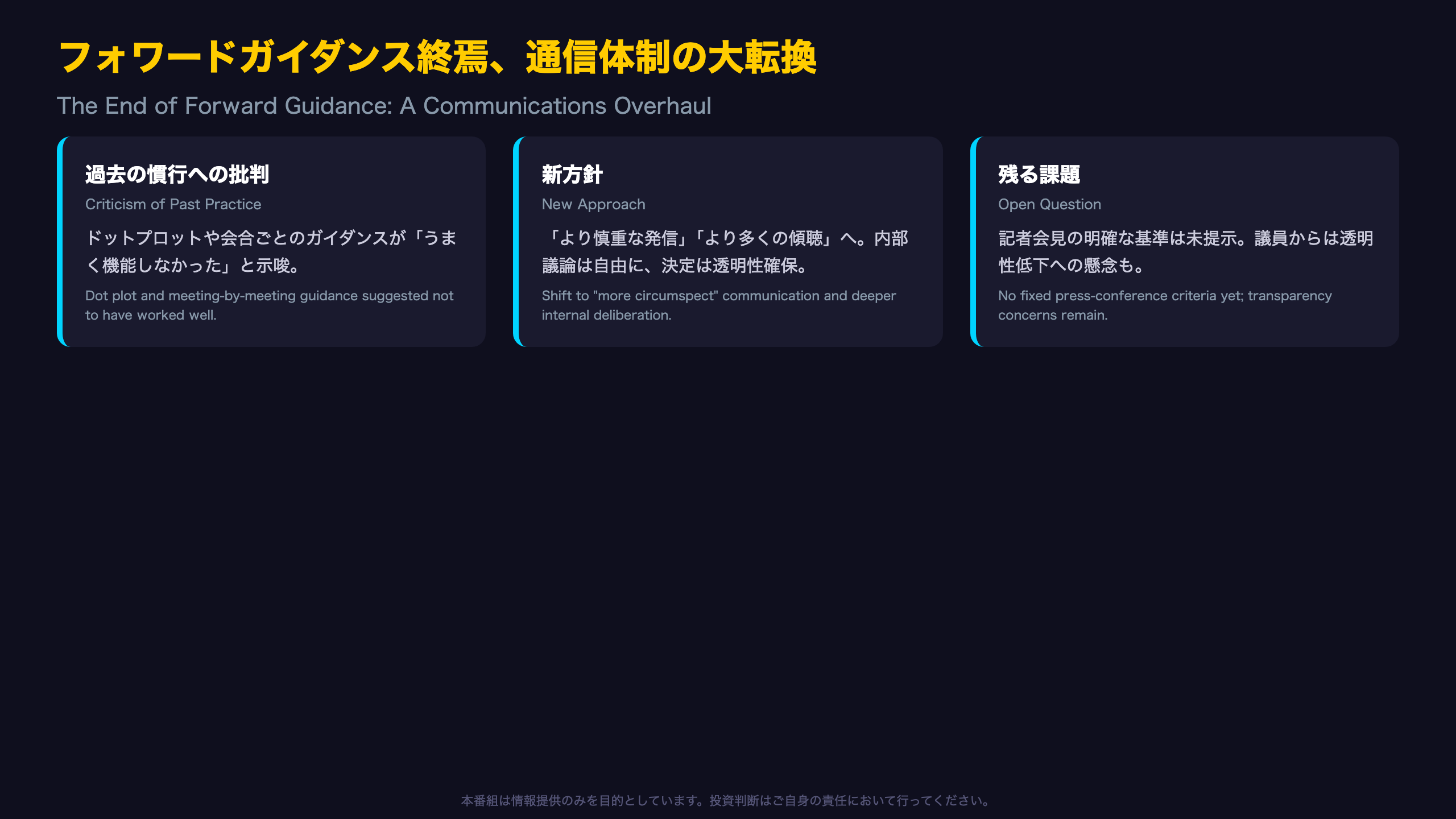

フォワードガイダンス終焉 — コミュニケーション体制の大転換

A Wall Street Journal Editorial Takes Center Stage

Rep. Andy Barr (R-KY) cited a June 15 Wall Street Journal editorial arguing that “few innovations since 2008 have been as counterproductive as the adoption of forward guidance,” claiming the quarterly Summary of Economic Projections (the “dot plot”) exposed “how little the Fed understands about the economy.” Warsh did not dispute this directly, framing communications reform as a “15-year” personal conviction rather than a new position.

The key quote

“If we were to give you my projection today about what we’ll do… we then find ourselves taking information that’s consistent with our priors and rejecting information that’s inconsistent.”

This is a notable admission that frequent public guidance can reinforce the Fed’s own confirmation bias — a risk rarely acknowledged so explicitly by a sitting chair.

The transparency pushback

Rep. Rashida Tlaib (D-MI) pushed back, warning that a “quieter Fed” risks becoming one “heard only by the well-connected.” Warsh drew a distinction: internal deliberations can stay freer and more candid, but final decisions, he said, “should be things you know everything about.”

For international readers

The Fed’s dot plot has no direct equivalent at the ECB, which relies on staff macroeconomic projections rather than individual policymaker rate paths — a structural difference that may inform how U.S. markets adjust to reduced Fed guidance relative to European peers.

What’s next

The communications task force is expected to report by year-end; the specific bar for triggering a press conference was deferred to a written follow-up response.

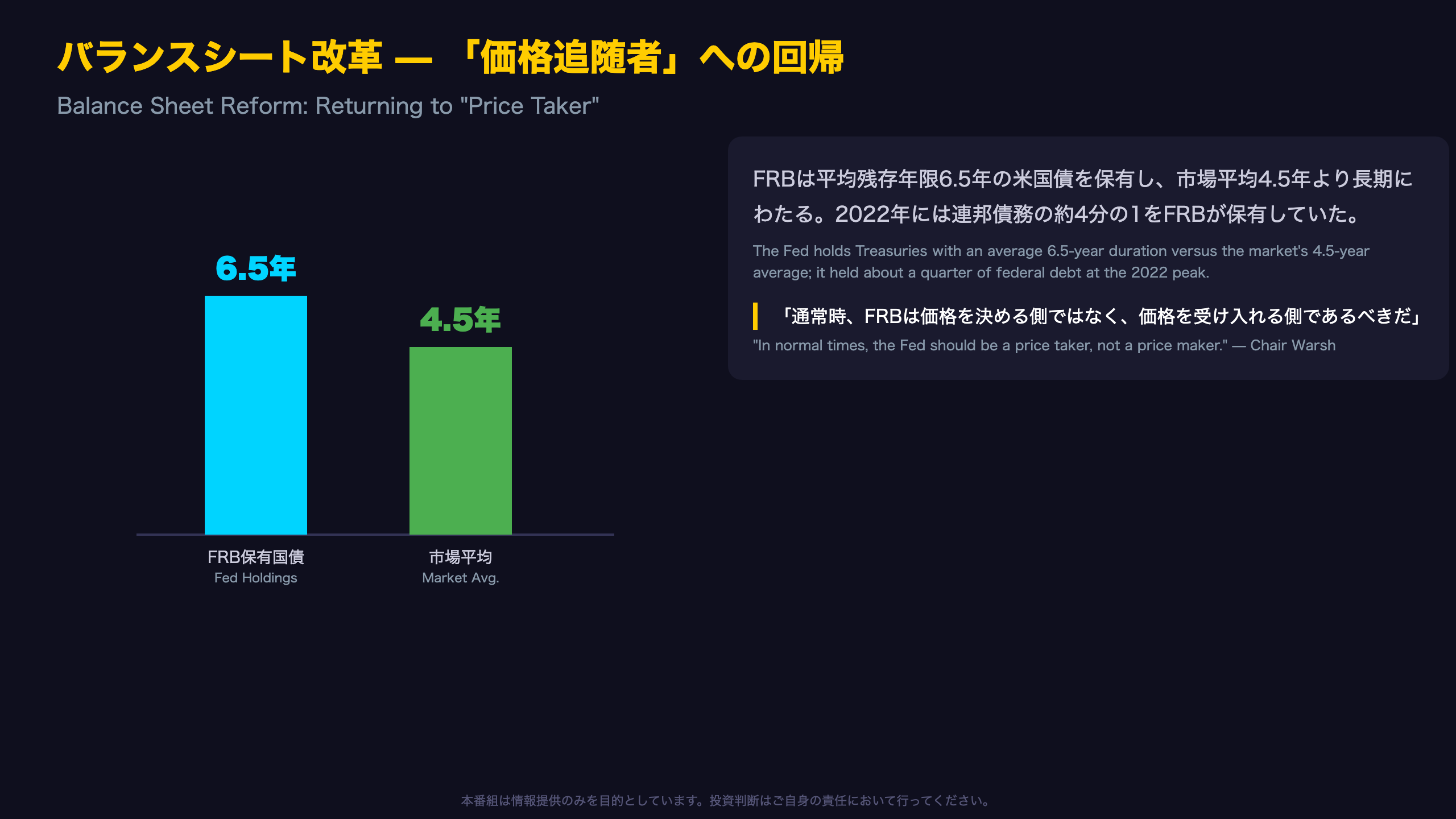

バランスシート改革 — 「価格追随者」への回帰

“The Balance Sheet Isn’t Merely About Plumbing”

Warsh outlined three principles for balance sheet policy: first, “the balance sheet is part of monetary policy… [it] isn’t merely about plumbing”; second, any change would be “previewed, explained, debated” well in advance; third, the Fed must “stay clear of fiscal policy.”

The duration mismatch

The Fed’s average Treasury holding duration is about 6.5 years, compared with roughly 4.5 years for the broader Treasury market — meaning the Fed disproportionately holds longer-dated debt. Warsh described this, borrowing from former Chair Paul Volcker, as being “on the edge of [monetary policy’s] authority.”

The 2022 peak and fiscal discipline

At its peak in 2022, the Fed held roughly a quarter of outstanding federal debt. While that share has since declined, Warsh argued that having such a large, reliable buyer “creates incentives for fiscal policymakers to avoid the tough decisions on debt and deficits.”

Competing views

Defenders of quantitative easing emphasize its effectiveness during genuine crises like 2008 and 2020. Reform-minded voices like Warsh instead focus on the side effects of prolonged QE well after crises ended — asset price distortion and weakened fiscal discipline in Congress.

What’s next

The balance sheet task force is examining size, composition, and the transition process. Warsh pledged that any eventual runoff or restructuring would come only with extensive advance notice — ruling out an abrupt shift for now.

International comparison

The ECB and Bank of England have pursued their own quantitative tightening programs at markedly different paces, offering useful benchmarks for how aggressively the Fed might eventually shrink its balance sheet relative to global peers.

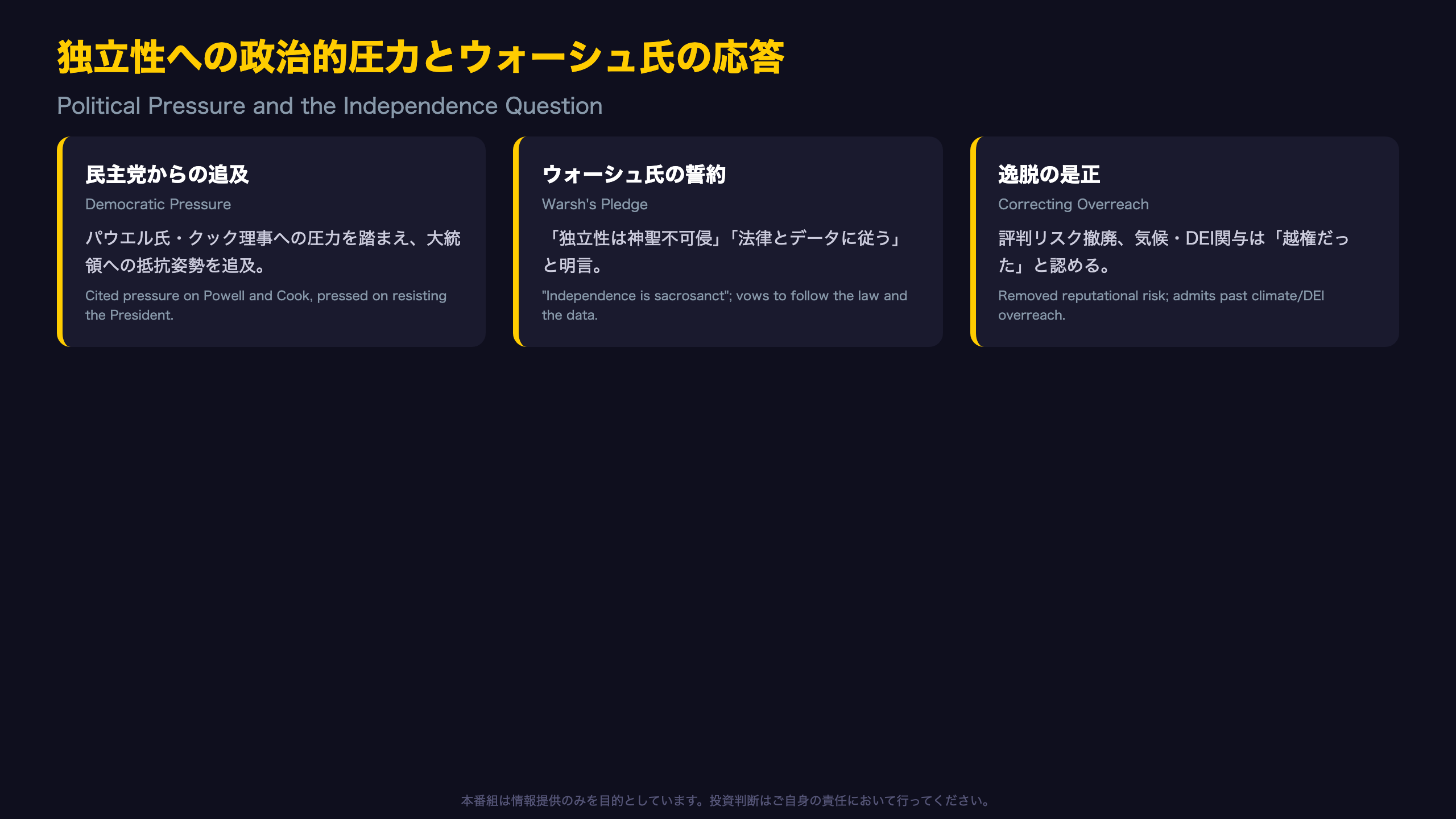

独立性への政治的圧力とウォーシュ氏の応答

The Specific Pledges

Rep. Meeks (D-NY) revisited a famous 2019 exchange in which then-Chair Powell was asked what he would do if the president tried to fire him and said he would refuse to comply. Warsh avoided a direct hypothetical but repeated his commitment to “follow the law and follow the data.” Rep. Foster (D-IL) pressed further, asking if Warsh would follow the data even amid public presidential criticism; Warsh answered simply, “I will.”

Removing “reputational risk”

Responding to Rep. Loudermilk’s (R-GA) question about “Operation Chokepoint 2.0,” Warsh confirmed that “reputational risk has been removed from the dashboard” supervisors use — formally distancing the Fed from a supervisory practice critics say was used to debank digital-asset and energy firms without statutory authority.

Stepping back from climate and DEI

In response to Rep. Barr (R-KY), Warsh effectively acknowledged that past Fed involvement in initiatives like the Network for Greening the Financial System fell outside its core mandate, stating, “our plate is full… we will not be wandering into other areas.”

A partisan asymmetry

Most independence-related questions came from Democratic members concerned about White House pressure on personnel and rate decisions, while Republican members focused chiefly on correcting past “mission creep” in supervision. This split in what each side considers the greater threat to Fed independence is likely to remain a recurring theme in future hearings.

Context for global readers

The U.S. Supreme Court’s 2025 ruling narrowing Humphrey’s Executor while carving out a partial shield for the Fed was referenced repeatedly — a legal backdrop with no direct parallel at the ECB or Bank of England, both of which operate under different constitutional independence frameworks.

市場へのインプリケーション

Three Market Implications, Traced Through the Chain of Evidence

1. Rates and FX

The Fed held its target range at 3.50-3.75% while repeating that “inflation is a choice” -> this reduces the odds markets price in near-term cuts -> suggesting the dollar and short-term yields could stay firmer for longer. This inference rests on a single hearing, however; the next FOMC meeting (described as “in a couple of weeks”) will be the more decisive confirmation point.

2. Equities and sector positioning

Equipment investment +8% and high-tech spending +25% -> suggests the AI-driven capex cycle remains intact -> this could support continued investor preference for capex-linked names such as semiconductors and data-center infrastructure.

3. Volatility

The move away from the dot plot and forward guidance -> makes the Fed’s meeting-by-meeting reaction function harder for markets to anticipate -> this could raise volatility around FOMC meetings. It is generally believed that increased central bank communication uncertainty raises bond term premia, though this testimony alone cannot confirm the magnitude of that effect.

A risk not to overlook

If housing weakness persists, softness among rate-sensitive consumers could partially offset the strength seen in investment-led sectors. Investors should watch the conclusions of the five task forces and the Fed’s actual policy decisions ahead of the next semi-annual testimony, typically held in February.

Bottom line for international investors

Unlike periods of clear forward guidance, markets may need to rely more heavily on incoming data (CPI, employment, capex figures) rather than Fed rhetoric to anticipate policy — a meaningful shift for global asset allocators positioned in U.S. rates and dollar assets.

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.