📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-07-08 09:19 JST)

📄 Primary Source

財務省

https://www.mof.go.jp/policy/international_policy/reference/balance_of_payments/preliminary/pg202605.htm

📊 Deep dive into Japan’s May 2026 Balance of Payments (MOF flash). Current account surplus widened to ¥3.97T (+¥648B YoY) 📈. Trade balance flipped back to surplus, exports up for a 9th straight month — but customs data show export volumes up just +0.4%, meaning the gains are mostly price effects from a weak yen (USD/JPY averaging 158.34) 💡. Services swung to deficit as inbound visitors fell -3.6% ⚠️. Primary income of ¥4.28T remains Japan’s true earnings engine. Plus: an eye-catching ¥11.4T drop in FX reserves. Balanced analysis of strengths and risks.

The Ultimate Summary:経常黒字3.97兆円へ拡大、ただし中身は二つの構造要因

Japan’s Current Account: The Big Picture

Japan’s Ministry of Finance (MOF) publishes monthly balance of payments data, and the May flash report shows a current account surplus of ¥3.97 trillion (roughly $25 billion at the month’s average rate of 158.34 yen per dollar), expanding ¥648 billion year-on-year.

For readers less familiar with Japan’s external accounts: unlike the US, which runs persistent current account deficits, Japan runs structural surpluses — but the composition has changed dramatically over the past decade. Japan no longer earns primarily through trade. Instead, primary income — dividends, interest, and reinvested earnings from Japan’s massive stock of overseas assets — is the dominant source, at ¥4.28 trillion this month alone.

Key takeaways for global investors

- The trade balance flipped back to a small surplus (¥6.9 billion) as exports rose 14.7% YoY, a ninth consecutive monthly gain.

- The services balance swung to a deficit of ¥10.3 billion as the travel surplus narrowed — a notable shift given Japan’s inbound tourism boom of recent years.

- Secondary income (transfers) improved by ¥190 billion, quietly contributing about 30% of the headline improvement.

Why it matters

A persistent current account surplus is generally considered a structural support for the yen over the medium term. However, much of Japan’s primary income is reinvested abroad rather than repatriated, so the actual yen-buying flow is smaller than the headline suggests. This distinction is central to understanding why the yen can stay weak despite large surpluses.

Deep Dive①:貿易黒字転化の分解——数量ではなく価格が動かした

What Customs Data Reveal: A Price-Driven Trade Recovery

Japan publishes two trade datasets: the balance-of-payments basis (MOF International Bureau) and the customs-clearance basis (MOF Customs Bureau). The customs data include volume/price decomposition, which is essential for judging the quality of the trade improvement.

The decomposition

- Exports: +16.8% in value, but only +0.4% in volume — prices contributed +16.4%

- Imports: +12.5% in value, with volumes down -6.8% and prices up +20.8%

For US-based readers: this is analogous to distinguishing real vs. nominal trade flows. Japan’s nominal trade boom is largely a currency and commodity price phenomenon, not a surge in real shipments. The yen averaged 158.34 per dollar in May, 9.4% weaker than a year earlier, while crude oil hit $114.66 per barrel (+52.2% YoY, +67.2% in yen terms).

Sector highlights

- Semiconductors and electronic components: exports +61.2% YoY — a genuine bright spot consistent with a global chip upcycle, as imports of the same category also jumped +55.0%.

- Autos: +13.7% in value but -2.3% in volume, meaning currency translation is doing the work.

Investor takeaway

The -6.8% drop in import volumes deserves attention: it may signal soft domestic demand or price-driven demand destruction, though a single month cannot confirm either. Meanwhile, the fact that Japan flipped to a trade surplus despite $114 oil suggests export pricing power is absorbing the commodity shock — a resilience signal that should not be dismissed.

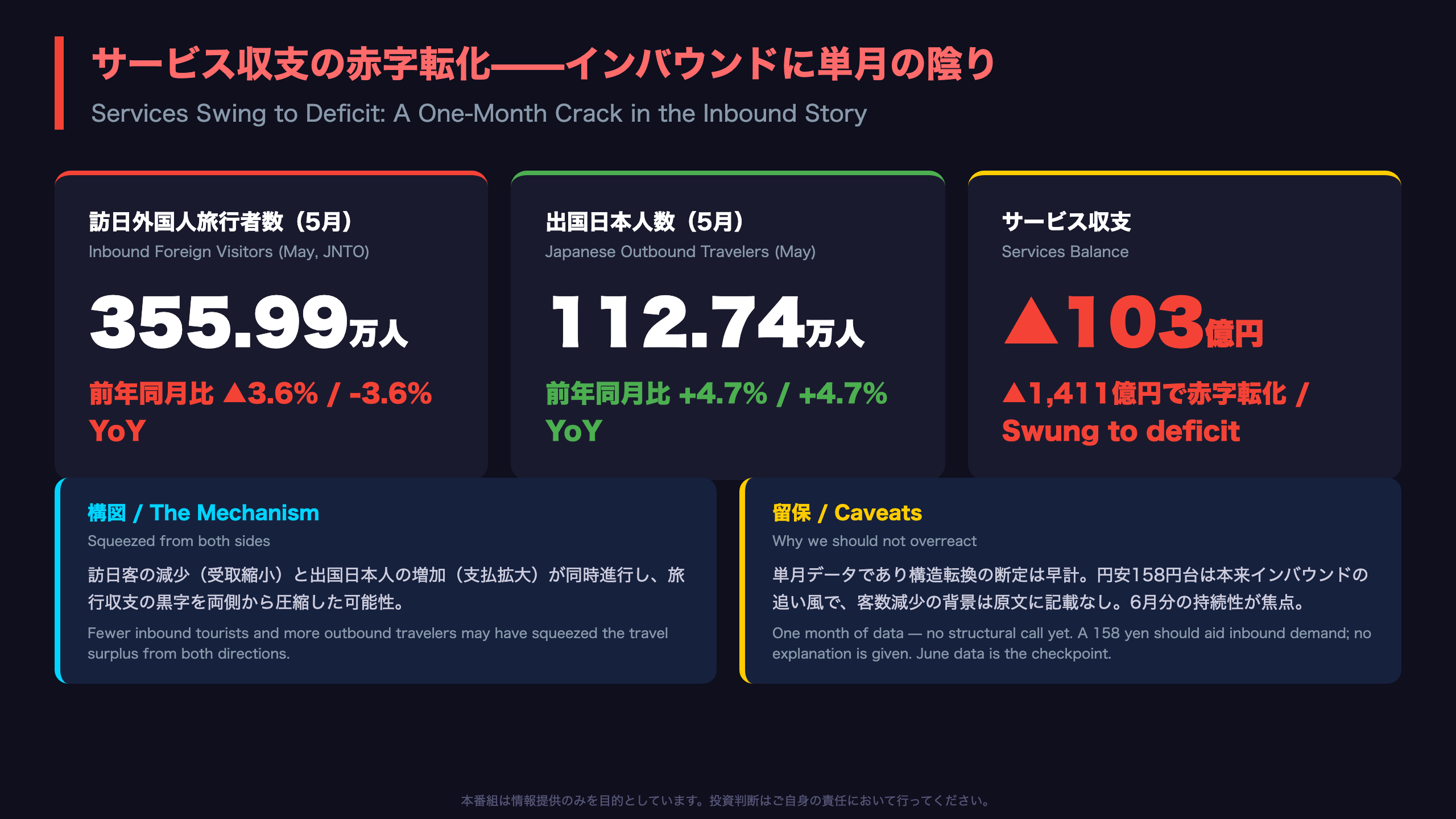

Deep Dive②:サービス収支の赤字転化——インバウンドに単月の陰り

Japan’s Travel Surplus Shows a Crack — Noise or Trend?

Japan’s services balance swung to a ¥10.3 billion deficit in May, and the MOF explicitly cites a narrower travel surplus as the main driver. For context: inbound tourism has been one of Japan’s biggest macro success stories, with the travel surplus acting as a counterweight to structural service deficits such as payments for foreign digital services (often dubbed Japan’s ‘digital deficit’ in domestic commentary).

The numbers

- Inbound visitors: 3,559,900 (-3.6% YoY) — per the Japan National Tourism Organization (JNTO), the government tourism agency

- Japanese outbound travelers: 1,127,400 (+4.7% YoY)

The travel account is being squeezed from both sides: fewer foreign tourists spending in Japan, and more Japanese residents spending abroad.

The puzzle

With the yen averaging 158 per dollar — near multi-decade lows in real terms — Japan should be exceptionally cheap for foreign visitors. A visitor decline in this environment is counterintuitive, and the report offers no explanation. Possible factors (capacity constraints, comparison-base effects) cannot be verified from this release alone.

What to watch

One month does not make a trend. The June JNTO visitor data and the next BoP release in early August are the checkpoints. For equity investors, sustained inbound softness would matter for Japanese retail, department store, hotel, and railway names that have been prime beneficiaries of the tourism boom. Conversely, recovering outbound travel hints at resilient Japanese household spending power — a mild domestic-demand positive often overlooked in bearish narratives.

Deep Dive③:第一次所得4.28兆円と、外貨準備▲11.4兆円という特異点

Inside the Financial Account: Three Capital Flow Stories

1. Primary income — Japan’s annuity

Japan holds the world’s largest net international investment position, and it shows: primary income (dividends, interest, and reinvested earnings from overseas assets) posted a ¥4.28 trillion surplus in a single month, driven by expanding securities investment income. For comparison, this month’s trade surplus was just ¥6.9 billion — three orders of magnitude smaller. Japan is structurally an investor nation, closer to a global asset manager than an export machine.

2. The ¥11.4 trillion FX reserve anomaly

The standout line item: official reserve assets fell by ¥11.4 trillion in May, a sharp reversal from +¥370 billion the prior month. The MOF report offers no explanation. Large reserve drawdowns are commonly associated with yen-buying currency intervention — Japan intervened in 2022 and 2024 episodes when the yen weakened sharply — and USD/JPY averaged 158.34 in May, 9.4% weaker YoY. However, valuation effects and portfolio shifts also move reserve balances, so this release alone cannot confirm intervention. Japan publishes monthly intervention data separately, which would be the definitive source.

3. Foreign appetite for Japanese assets

Inward equity investment showed net foreign buying of ¥2.17 trillion, which the MOF attributes specifically to buying in the banking sector — consistent with global investors positioning for Japanese financials. Inward investment in medium- to long-term bonds (mostly JGBs) also rose ¥598 billion. Meanwhile, trust banks — often a proxy for Japanese pension money — swung back to net buying of foreign bonds (+¥2.38 trillion), a notable flow reversal from the prior month’s heavy selling.

インプリケーション:根拠の鎖で読む為替・株式・注目点

Market Implications: Three Chains of Evidence

Chain 1: Current account and the yen

[¥3.97T surplus, +¥648B YoY] → [base for real-demand yen buying] → [medium-term yen support]

The caveat is critical: Japan’s surplus is dominated by primary income, much of which is reinvested abroad rather than repatriated. This is why the yen traded at 158 per dollar — near historic lows — even as the surplus expanded. The surplus is a slow-burning structural support, not a near-term catalyst. FX traders should weight the reserve data (below) more heavily.

Chain 2: Weak yen and corporate earnings

[Export volumes +0.4%, prices +16.4%] → [weak yen lifts yen-based export margins] → [potential support for Japanese manufacturers’ earnings]

This is the classic weak-yen equity story: Nikkei-listed exporters translate foreign revenue into more yen. The +61.2% surge in semiconductor exports, mirrored by +55% semiconductor imports, is consistent with a global chip upcycle — relevant for Japanese semiconductor equipment and materials names.

Chain 3: Inbound tourism and domestic sectors

[Visitors -3.6%, travel surplus narrowed] → [slower inbound consumption growth] → [potential headwind for retail, hotels, railways]

One month only — treat as a watch item, not a signal.

The wildcard: FX reserves

The ¥11.4 trillion reserve drop is the single most market-sensitive line in this report. If confirmed as intervention by the MOF’s separate intervention disclosure, it would signal the authorities’ tolerance limit for yen weakness near 158 — directly relevant for USD/JPY positioning. Next checkpoints: the MOF intervention data and the June BoP release in early August.

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.