📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-06-25 02:40 JST)

📄 Primary Source

Bank of Canada

https://www.bankofcanada.ca/2026/06/summary-of-governing-council-deliberations-fixed-announcement-date-of-june-10-2026/

Deep dive into the Bank of Canada’s June 10, 2026 meeting minutes (published June 25). The Governing Council held rates at 2.25% but explicitly flagged a two-sided policy dilemma: cut rates to support a weak economy, or hike to prevent energy-driven inflation from becoming entrenched. We break down the key debates, the three major risk scenarios, and what the minutes signal for the next BOC decision.

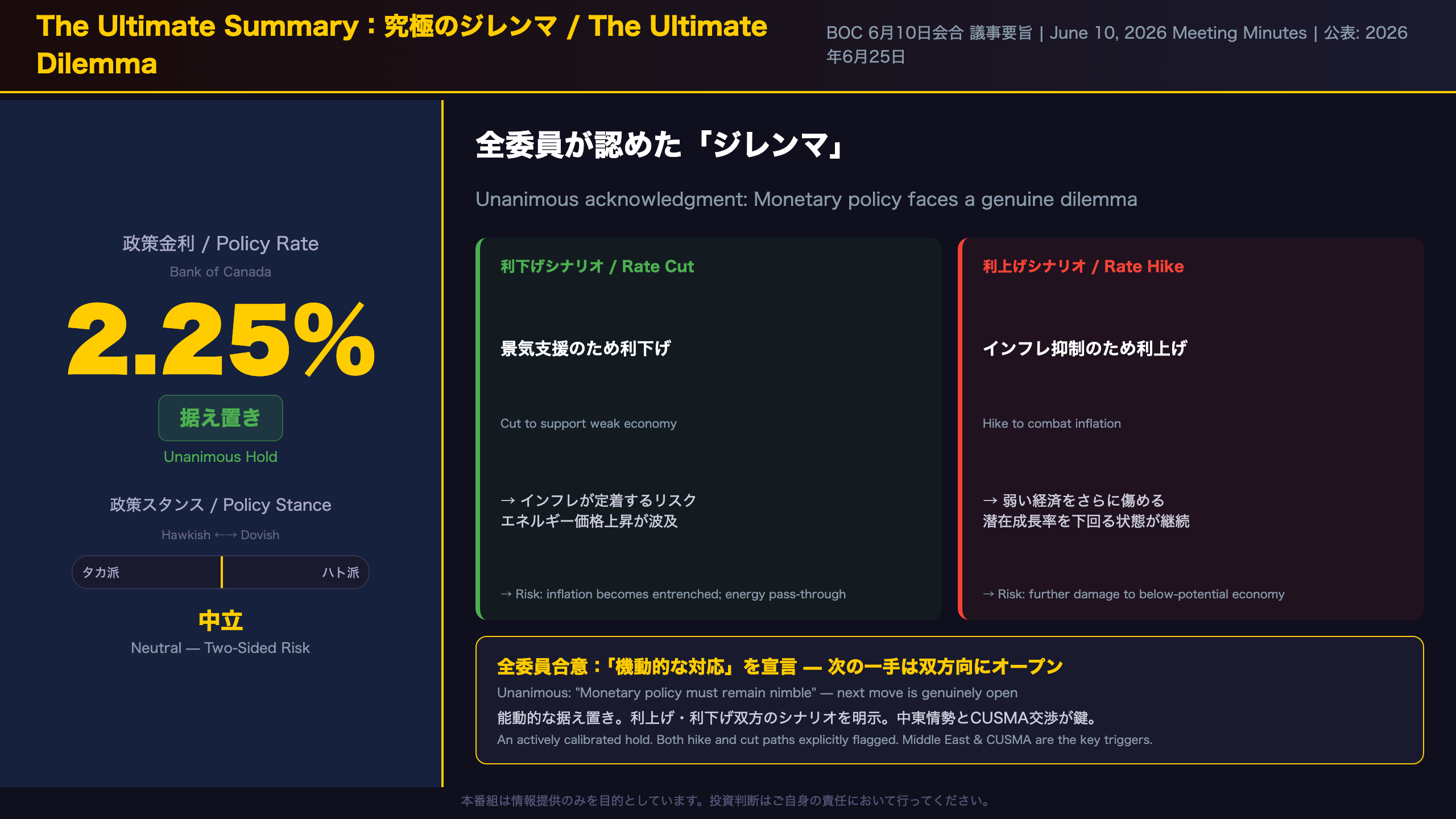

The Ultimate Summary:究極のジレンマと「据え置き」の意味

The Key Takeaway: An Explicit Dilemma

The most significant aspect of the Bank of Canada’s June 2026 minutes is the unanimous acknowledgment by all Governing Council members that monetary policy faces a genuine dilemma. This represents a meaningful shift in tone from the April minutes, where the hold decision was framed more straightforwardly as “appropriate.”

What Is the Bank of Canada’s Governing Council?

The Bank of Canada (BOC) is Canada’s central bank, responsible for monetary policy and price stability. Its Governing Council — the equivalent of the Fed’s FOMC — consists of the Governor, Senior Deputy Governor, and four Deputy Governors. Unlike the Fed, individual dissents are not publicly disclosed; the minutes reflect collective deliberations.

The Two-Sided Dilemma

The Council explicitly framed the policy challenge as follows:

- Cutting rates to support a weak economy (Q1 GDP: -0.1%) risks allowing energy-driven inflation to become entrenched in pricing behavior

- Hiking rates to combat inflation (CPI at 2.8% in April) risks further damaging an economy already operating below potential

This is a classic stagflationary dilemma — weak growth coinciding with above-target inflation driven by an external supply shock (Middle East conflict → higher oil prices).

Comparison with April Minutes

| Dimension | April Meeting | June Meeting |

|---|---|---|

| Policy Rate | 2.25% (hold) | 2.25% (hold) |

| Tone | “Current stance appropriate” | “Dilemma” explicitly stated |

| GDP Outlook | Expected Q1 recovery | Q1 came in at -0.1% |

| Core Inflation | Easing momentum | Near 2%, limited pass-through |

| Policy Bias | Mildly neutral | Genuinely two-sided |

The hold decision is best understood not as inaction, but as an actively calibrated pause while the Council waits for clearer signals on whether inflation is broadening or whether trade risks are materializing.

国内経済の現状:「弱いがリセッションではない」

“Weak But Not in Recession”: The Council’s Economic Assessment

The Q1 GDP Miss

The most concrete data point in the June minutes was the Q1 2026 GDP figure: -0.1% quarter-over-quarter, a massive 1.6 percentage point miss versus the +1.5% forecast in the April Monetary Policy Report (MPR).

The MPR is the Bank of Canada’s quarterly flagship publication — equivalent to the Fed’s Summary of Economic Projections — where the Governing Council publishes its official economic forecasts. The April MPR had projected a solid Q1 recovery after Q4 2025’s contraction.

What Drove the Miss?

The primary culprit was a 2.5% drop in government spending, mainly driven by a large quarterly decline in weapons systems procurement. Members explicitly noted that government spending patterns “can be choppy from one quarter to the next” — suggesting they view this as a one-off rather than a structural deterioration.

The Resilient Consumer

In contrast to the headline GDP miss, consumer spending grew +1.4% in Q1, with per-capita consumption up +2%. This is a meaningful positive signal: even as population growth slows, individual Canadians are continuing to spend.

Labour Market: Volatile but Not Collapsing

May employment surprised to the upside, pulling the unemployment rate down to 6.6%. However, the Council was careful to flag that employment data has been volatile — employment is little changed since January, and the unemployment rate has been oscillating in a 6.5%–7.0% range for several months.

The Recession Debate

The Council explicitly addressed whether Canada is in recession, defining it as “a deep, widespread and persistent decline in aggregate economic activity.” Their conclusion: not yet. While GDP was barely negative in Q1 and contracted in Q4 2025, more than half of industries recorded some growth — failing the “widespread” criterion. This is an important distinction for investors: the economy is weak and operating below potential, but the Council does not see a recession as the base case.

インフレ認識:エネルギー価格の波及は限定的、コアは2%近辺

Inflation Assessment: “Core Near 2%, But Monitoring Required”

April CPI: 2.8% — Slightly Below Forecast

April CPI came in at 2.8% year-over-year, marginally below the Bank’s own forecast of “around 3%” from the April MPR. Two factors drove the increase:

- Gasoline price surge: Direct impact of Middle East conflict on energy prices

- Carbon tax base effect: Last April’s elimination of the consumer carbon tax dropped out of the 12-month comparison, mechanically pushing up the year-over-year rate

Core Inflation: The More Important Signal

The Bank of Canada uses two preferred core inflation measures — CPI-trim (which trims the tails of the price distribution) and CPI-median (the price change at the 50th percentile of the distribution). Both are analogous to the Fed’s “core PCE” as preferred measures of underlying inflation.

Both CPI-trim and CPI-median fell close to 2% in April — the Bank’s inflation target. This is a meaningful positive signal: despite headline CPI at 2.8%, underlying price pressures are well-contained.

Pass-Through Assessment

| Inflation Component | Status | Trend |

|---|---|---|

| Headline CPI | 2.8% | Rising (energy) |

| CPI-trim | ~2% | Declining |

| CPI-median | ~2% | Declining |

| Share of items >3% | Near historical avg | Declining |

| Food inflation | Elevated but easing | Improving |

| Rent inflation | Slowing further | Improving |

Why Limited Pass-Through?

The Council’s assessment that energy price pass-through is limited is consistent with the broader economic picture: the economy is operating in excess supply with slack in the labour market. When demand is weak, businesses have less pricing power and are less able to pass on higher input costs to consumers.

The Key Risk: Persistence

The Council explicitly flagged that if supply chain disruptions and Middle East uncertainty persist, “backlogs and bottlenecks could persist.” The trigger for policy tightening is clear: evidence that inflation pressures are spreading or becoming more persistent.

政策判断の核心:「過剰反応」vs「対応遅れ」のトレードオフ

The Over-Tightening vs. Under-Tightening Trade-Off

This section of the June minutes represents the most intellectually substantive policy debate. The Governing Council explicitly compared two types of policy timing errors.

Scenario A: Over-Tightening

The Council noted: “If the Bank were to raise rates to combat higher inflation and oil prices came back down quickly, by the time higher interest rates were affecting the economy, they would not be needed.”

Monetary policy operates with a lag of typically 6–18 months. Hiking now to combat energy-driven inflation risks tightening into a slowdown — a classic policy error. If oil prices normalize quickly (e.g., Middle East ceasefire holds), the inflation impulse fades on its own, and the rate hikes would only serve to deepen the economic weakness.

Scenario B: Under-Tightening

Conversely: “But if higher oil prices persisted and spread, and the Bank held the policy rate for too long, the eventual monetary policy response would have to be more aggressive than if it had acted earlier.”

This is the 2021–2022 lesson: central banks that were too slow to respond to inflation ultimately had to hike more aggressively, causing greater economic disruption. The Council is clearly aware of this risk.

The Decision: Conditional Look-Through

Faced with this asymmetric risk, members agreed to look through the near-term inflation impact of higher energy prices — but with explicit conditions:

Conditions for maintaining the look-through:

– Economy operating in excess supply

– Core inflation measures near 2%

– Limited evidence of energy price pass-through

– Policy rate at the stimulative end of the neutral range

Trigger for abandoning the look-through (→ hike):

– Inflation data showing broadening or persistence

– Evidence of pass-through to non-energy goods and services

– Inflation expectations becoming unanchored

This conditional framework is more sophisticated than a simple hold — it’s a data-dependent, trigger-based pause with clearly defined escalation criteria.

3つのシナリオと次回政策アクションの条件

Three Scenarios: The Conditions Map for the Next Policy Move

The most actionable content in the June minutes is the explicit mapping of conditions for future policy actions. The Governing Council laid out three distinct scenarios.

Scenario 1: Rate Cut (Downside Risk Materializes)

Trigger: US imposes new trade restrictions on Canada

Mechanism: Trade restrictions → sharp decline in exports and investment → accelerating economic weakness → rate cut to support growth

The CUSMA (Canada-United States-Mexico Agreement) review is currently underway. Members noted that “if negotiations are prolonged and particularly if the outcome is unfavourable, hardship in trade-affected sectors could deepen and spread, and the effects on jobs and investment could be felt more broadly through the Canadian economy.”

Scenario 2: Consecutive Rate Hikes (Upside Risk Materializes)

Trigger: Middle East conflict continues → high energy prices lead to generalized inflation

Mechanism: Persistent energy prices → supply chain disruptions → inflation expectations rise → consecutive hikes needed

The word “consecutive” is significant — this implies multiple rate increases, not a single adjustment. This is the more hawkish scenario.

Scenario 3: Both Risks Simultaneously (Most Complex)

Trigger: US trade restrictions AND prolonged Middle East conflict

This creates a stagflationary dynamic — economic weakness (arguing for cuts) coinciding with rising inflation (arguing for hikes). The Council explicitly did not rule out this possibility, stating: “It is also possible that both risks could materialize at the same time. Monetary policy will need to remain nimble.”

Comparison with April Minutes

The April minutes presented a similar three-scenario framework. The key difference in June is the explicit use of the word “dilemma” and the acknowledgment that the economy has underperformed expectations — making the trade-offs more acute.

Market Implication

The Canadian dollar has depreciated against the USD, reflecting market expectations that the gap between Canadian and US interest rates could be more persistent than previously anticipated. This is consistent with the downside scenario (rate cut) being assigned meaningful probability by markets — though the minutes themselves do not quantify probabilities.

インプリケーション:市場・為替・次回政策への示唆

Market Implications: The “Chain of Evidence” Framework

Canadian Dollar (CAD/USD)

Chain of evidence: The minutes explicitly stated that “the Canadian dollar has depreciated against the US dollar, reflecting weaker economic data and market expectations that the gap between Canadian and US interest rates could be more persistent than previously anticipated” → This suggests markets are assigning meaningful probability to the BOC cutting rates while the Fed holds or hikes → CAD depreciation pressure may persist.

Counter-scenario: If the Middle East conflict resolves and oil prices fall, Canada as an energy exporter would benefit, potentially supporting CAD. This is generally considered a positive correlation between CAD and oil prices, but cannot be confirmed from this document alone.

Canadian Government Bonds

Chain of evidence: The next policy move is genuinely open — both hike and cut scenarios are explicitly on the table → Uncertainty about the direction of rates is elevated → Canadian bond yield volatility may increase as incoming data shifts the balance of risks.

Canadian Equities

Chain of evidence: “Financial conditions had loosened, with strength in equity markets and little change in bond yields” → Near-term backdrop is neutral to mildly supportive for equities.

Risk: If CUSMA negotiations produce an unfavorable outcome, trade-exposed sectors (autos, agriculture, manufacturing) could face significant headwinds.

Key Watchpoints Before the July 2026 Meeting

| Indicator | What to Watch | Implication |

|---|---|---|

| Middle East | Ceasefire durability; Strait of Hormuz reopening | Oil price direction |

| CUSMA | Negotiation progress; US posture | Trade restriction risk |

| June CPI | Energy pass-through to non-energy items | Hike trigger |

| Q2 GDP | Confirmation of April flash +0.4% MoM | Recession risk |

| Business surveys | Investment and hiring intentions | Forward-looking demand |

The BOC’s next scheduled decision is in July 2026. The minutes make clear that the Bank is in a genuine data-dependent mode — the next move could be in either direction.

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.