📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-06-29 18:10 JST)

📄 Primary Source

Bank of England

https://www.bankofengland.co.uk/statistics/money-and-credit/2026/may-2026

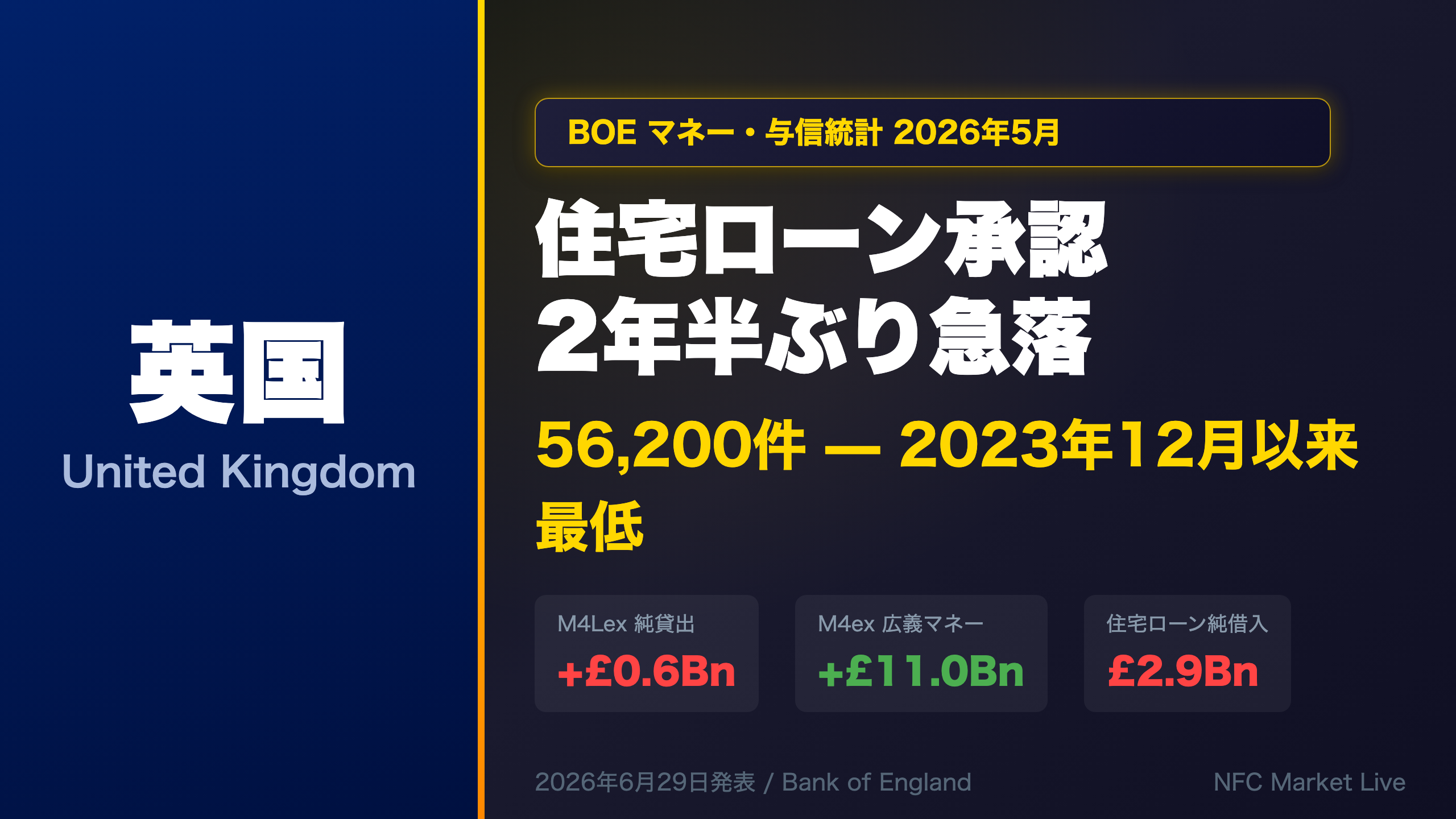

Deep dive into the Bank of England’s Money and Credit release for May 2026 (published June 29, 2026). Mortgage approvals plunged to 56,200 — the lowest since December 2023. M4Lex net lending collapsed to just £0.6bn from £11.5bn in April. Yet broad money M4ex expanded to £11.0bn and consumer credit annual growth ticked up to 8.9%. We unpack the divergence between money supply and credit demand, and what it means for BOE rate policy and GBP.

The Ultimate Summary: 住宅市場に急ブレーキ、与信は二極化

May 2026 UK Money & Credit: Housing Cools Sharply While Consumer Credit Holds Firm

The Bank of England’s Monthly Release — Context for International Readers

The Bank of England publishes its Money and Credit statistical release monthly, covering broad money supply (M4ex), net lending to the private sector (M4Lex), mortgage approvals, consumer credit, and business borrowing. This data is closely watched by the BOE’s Monetary Policy Committee (MPC) as a real-time gauge of credit conditions and monetary transmission.

The Headline Shock: Mortgage Approvals at a 2.5-Year Low

Mortgage approvals for house purchases fell to 56,200 in May — the lowest since December 2023 (52,600) and well below the six-month average of 63,300. This is a leading indicator of future mortgage borrowing and housing market activity. The drop suggests that higher mortgage rates (effective rate on new mortgages rose to 4.22% in May from 4.08% in April) are increasingly weighing on housing demand.

The Divergence: Money Supply vs. Credit Demand

The most analytically interesting feature of this release is the divergence between M4ex (broad money, which rose to £11.0bn) and M4Lex (net lending, which collapsed to just £0.6bn from £11.5bn in April). This gap suggests that money is circulating in the financial system but is not being channeled into new credit — a pattern that could reflect risk aversion among borrowers or lenders, or both.

Implications for BOE Rate Policy and GBP

- Dovish signal: The housing market slowdown and M4Lex collapse provide ammunition for MPC members favoring further rate cuts.

- Hawkish counterweight: Consumer credit annual growth of 8.9% and accelerating M4ex suggest household spending capacity remains intact, keeping inflation risks alive.

- For GBP: The mixed picture creates uncertainty. A sustained housing downturn could weigh on GBP if it shifts market pricing toward more aggressive BOE easing.

住宅市場の急冷:承認件数と純借入の急落

UK Housing Market Deep Dive: Approvals at a 2.5-Year Low

Context: What Are Mortgage Approvals?

In the UK, the Bank of England tracks net mortgage approvals (approvals minus cancellations) for house purchases as a leading indicator of future mortgage borrowing and housing market activity. This is broadly analogous to the US Pending Home Sales Index in its forward-looking nature.

The Numbers in Detail

Mortgage approvals for house purchases fell to 56,200 in May — down 15% from April’s 66,000 and the lowest since December 2023 (52,600). The six-month average stands at 63,300, meaning May’s reading is approximately 11% below trend.

Remortgage approvals (capturing borrowers switching to a different lender) also fell sharply, from 51,200 in April to 33,300 in May — a 35% single-month decline. This may reflect borrowers pausing remortgage decisions in anticipation of further BOE rate cuts, though this interpretation requires caution given single-month data.

The Repayment Surge

A notable feature of this release is that gross lending (£27.1bn) remains above the six-month average (£25.3bn), yet net borrowing (£2.9bn) is well below average. The gap is explained by surging repayments (£22.9bn vs. six-month average of £19.9bn). This suggests existing mortgage holders are accelerating repayments — a rational response to elevated borrowing costs.

International Comparison

The effective rate on new UK mortgages rose to 4.22% in May. For context, the average 30-year fixed mortgage rate in the US was around 6.8-7.0% during the same period, making UK mortgage rates relatively lower — yet the UK housing market appears more sensitive to rate changes, partly due to the prevalence of shorter fixed-rate terms (2-5 years) in the UK versus the US 30-year fixed norm.

Key Threshold to Watch

If June approvals (to be released July 29) fall below 56,200, it would confirm a structural downtrend in housing demand — a significant signal for BOE policy and UK real estate markets.

M4Lex急収縮の解剖:NIOFCsの大規模返済が主因

Dissecting the M4Lex Collapse: NIOFCs and Real Economy Implications

What Is M4Lex?

M4Lex (M4 Lending Excluding Intermediate OFCs) measures net sterling lending by UK monetary financial institutions (MFIs) to the private sector, broken down by sector: households, private non-financial corporations (PNFCs), and non-intermediate other financial corporations (NIOFCs). It is the BOE’s preferred measure of credit conditions in the real economy.

The NIOFC Swing: Financial Sector Noise or Signal?

The dominant driver of May’s M4Lex collapse was NIOFCs, which swung from £2.1bn net borrowing in April to £6.9bn net repayment in May — a £9.0bn reversal. NIOFCs include hedge funds, securities dealers, and special purpose vehicles. Their borrowing patterns are highly volatile on a monthly basis, often reflecting short-term repo transactions, fund restructuring, or end-of-quarter positioning rather than underlying economic conditions.

This means the headline M4Lex figure of £0.6bn should be interpreted with significant caution. Stripping out NIOFCs, the real-economy M4Lex (households + PNFCs) was approximately £6.4bn — still below April’s £9.4bn but far less alarming than the headline figure suggests.

Real Economy Credit: Softening but Not Collapsing

| Sector | May | April | Change |

|---|---|---|---|

| NIOFCs | -£6.9bn (repayment) | +£2.1bn | -£9.0bn |

| Households | +£4.2bn | +£5.0bn | -£0.8bn |

| PNFCs | +£2.2bn | +£4.4bn | -£2.2bn |

| Total M4Lex | +£0.6bn | +£11.5bn | -£10.9bn |

Annual Growth Rate: A More Stable Signal

The annual growth rate of M4Lex declined to 5.9% from 6.4% in April. This smoother series is less affected by monthly NIOFC volatility and may be a more reliable indicator of the underlying credit trend. A reading of 5.9% still represents positive credit growth, though the direction of travel is downward.

M4exの拡大と消費者信用の底堅さ:強さのシグナル

M4ex Expansion and Resilient Consumer Credit: Reading the Strength Signals

M4ex: Broad Money Continues to Expand

M4ex annual growth accelerated to 4.8% in May from 4.6% in April, with monthly flows rising from £9.2bn to £11.0bn. This indicates that liquidity in the UK financial system continues to expand — a broadly supportive backdrop for economic activity.

Household Deposits: ISA Season Normalization

April’s household deposit data was distorted by the UK tax year-end (April 5th), which triggered a surge of ISA (Individual Savings Account) contributions — £12.0bn in April vs. £3.1bn in May. ISAs are tax-advantaged savings accounts in the UK, broadly analogous to US Roth IRAs or Canadian TFSAs. The May normalization is therefore a seasonal correction, not a structural shift in saving behavior.

Notably, the effective rate on new time deposits rose to 4.26% in May from 4.07% in April — the highest in recent months. This suggests households are actively seeking yield in fixed-term deposits, consistent with a “higher for longer” rate environment.

Consumer Credit: Resilient but Nuanced

Consumer credit annual growth rose to 8.9% from 8.7%, with credit card growth at 12.1% and other forms (car finance, personal loans) at 7.5%. For international context, UK consumer credit growth of ~9% is notably higher than the US (~5-6% in the same period), suggesting UK households are maintaining spending through borrowing.

Two interpretations exist:

– Bullish read: Strong consumer demand supports economic growth and reduces recession risk.

– Cautious read: High credit growth may reflect households borrowing to maintain living standards amid cost-of-living pressures — a sign of financial stress rather than confidence.

The BOE will need to weigh both interpretations when assessing the inflation outlook.

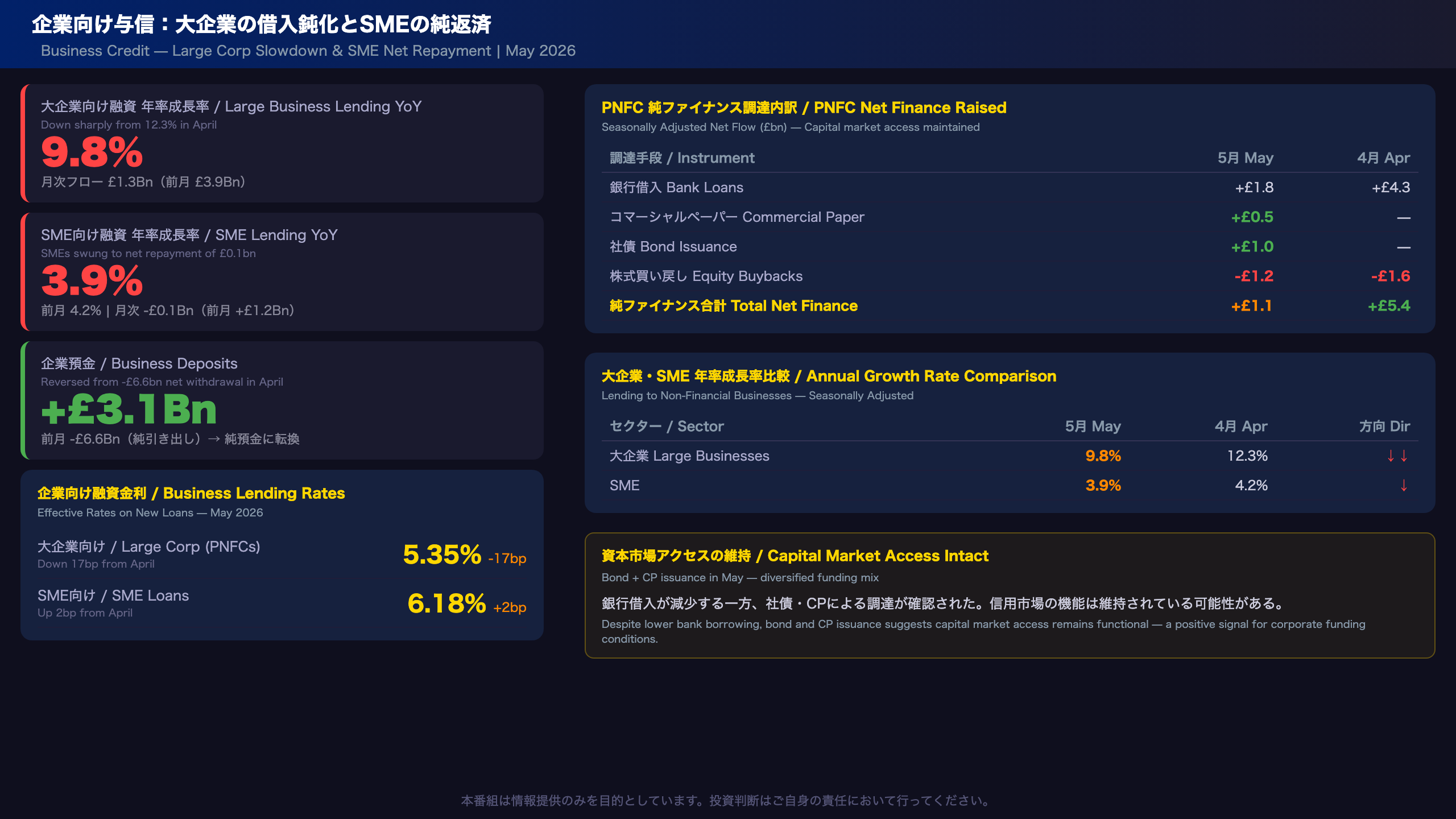

企業向け与信:大企業の借入鈍化とSMEの純返済

Business Credit Deep Dive: Borrowing Slowdown and Capital Market Access

Large Business Lending: Annual Growth Rate Drops Sharply

The annual growth rate of lending to large businesses fell from 12.3% in April to 9.8% in May — a 2.5 percentage point drop in a single month. Monthly flows also fell sharply from £3.9bn to £1.3bn. While this may suggest large corporates are pulling back on bank borrowing, caution is warranted given single-month data.

SMEs: From Net Borrowing to Net Repayment

SMEs swung from £1.2bn net borrowing in April to £0.1bn net repayment in May. The annual growth rate edged down from 4.2% to 3.9%. UK SMEs are particularly sensitive to borrowing costs given their reliance on variable-rate bank lending, and the effective rate on new SME loans was 6.18% in May — notably higher than the 5.35% rate for large corporates.

Business Deposits: A Positive Reversal

Non-financial businesses deposited a net £3.1bn in May, reversing April’s £6.6bn net withdrawal. This improvement in business liquidity is a positive signal, suggesting corporate cash positions may be stabilizing.

PNFC Capital Market Access: Diversified Funding

Despite the drop in bank borrowing, PNFCs raised £1.0bn through bond issuance and £0.5bn through commercial paper in May — channels that were not utilized in April. This suggests that capital market access remains intact, and corporates are diversifying their funding mix away from bank loans. The effective rate on new PNFC bank loans fell 17 basis points to 5.35% in May, which may attract more bank borrowing in coming months if demand recovers.

Rate Differential: Large vs. SME

The 83 basis point spread between large corporate (5.35%) and SME (6.18%) borrowing rates highlights the ongoing financing cost disadvantage faced by smaller businesses — a structural feature of UK credit markets that the BOE monitors closely.

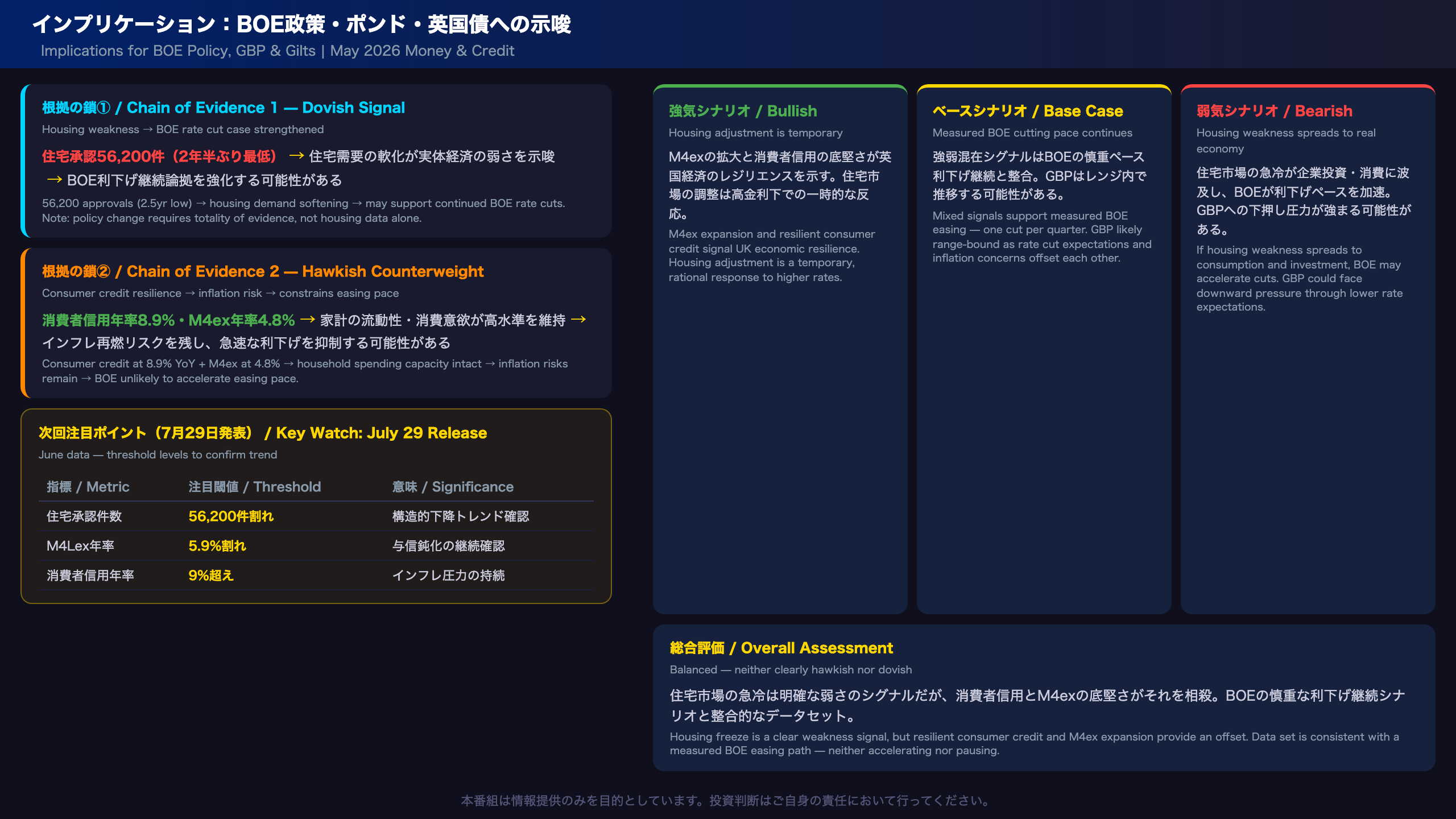

インプリケーション:BOE政策・ポンド・英国債への示唆

Market Implications: Following the Chain of Evidence

Chain 1: Housing → BOE Rate Cuts → GBP

[Mortgage approvals at 56,200 — lowest since Dec 2023] → [Signals softening housing demand and potential real economy weakness] → [May strengthen the case for continued BOE rate cuts]

However, whether housing weakness alone triggers a change in BOE policy depends on the totality of evidence including inflation, employment, and wage data. It is generally understood that housing market weakness raises rate cut expectations and weighs on GBP, but this data alone is insufficient to make that determination with confidence.

Chain 2: Consumer Credit → Inflation → BOE Caution

[Consumer credit annual growth at 8.9%, M4ex at 4.8%] → [Household liquidity and spending capacity remain elevated] → [Keeps inflation risks alive, potentially constraining the pace of BOE easing]

Scenario Analysis

Base case (most likely): BOE continues cutting rates at a measured pace — one cut per quarter. Housing weakness supports easing; consumer credit resilience prevents acceleration. GBP remains range-bound.

Dovish scenario: If June mortgage approvals fall below 56,200 and M4Lex annual growth continues to decline, the BOE may signal a faster easing path. GBP could face downward pressure.

Hawkish scenario: If consumer credit growth accelerates above 9% and M4ex growth continues to rise, the BOE may pause its cutting cycle. GBP could find support.

Key Dates

- July 29, 2026: Next Money and Credit release (June data)

- August 7, 2026: Next BOE MPC decision (approximate)

For International Investors

The divergence between a cooling housing market and resilient consumer credit is a pattern seen in other advanced economies navigating the post-tightening cycle. The key question is whether housing weakness is a leading indicator of broader economic slowdown, or whether it remains contained while consumption holds up. This release does not resolve that question — it raises it.

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.