📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-06-24 17:00 JST)

📄 Primary Source

Sveriges Riksbank

https://www.riksbank.se/en-gb/press-and-published/notices-and-press-releases/press-releases/2026/minutes-of-the-monetary-policy-meeting-on-16-june-2026/

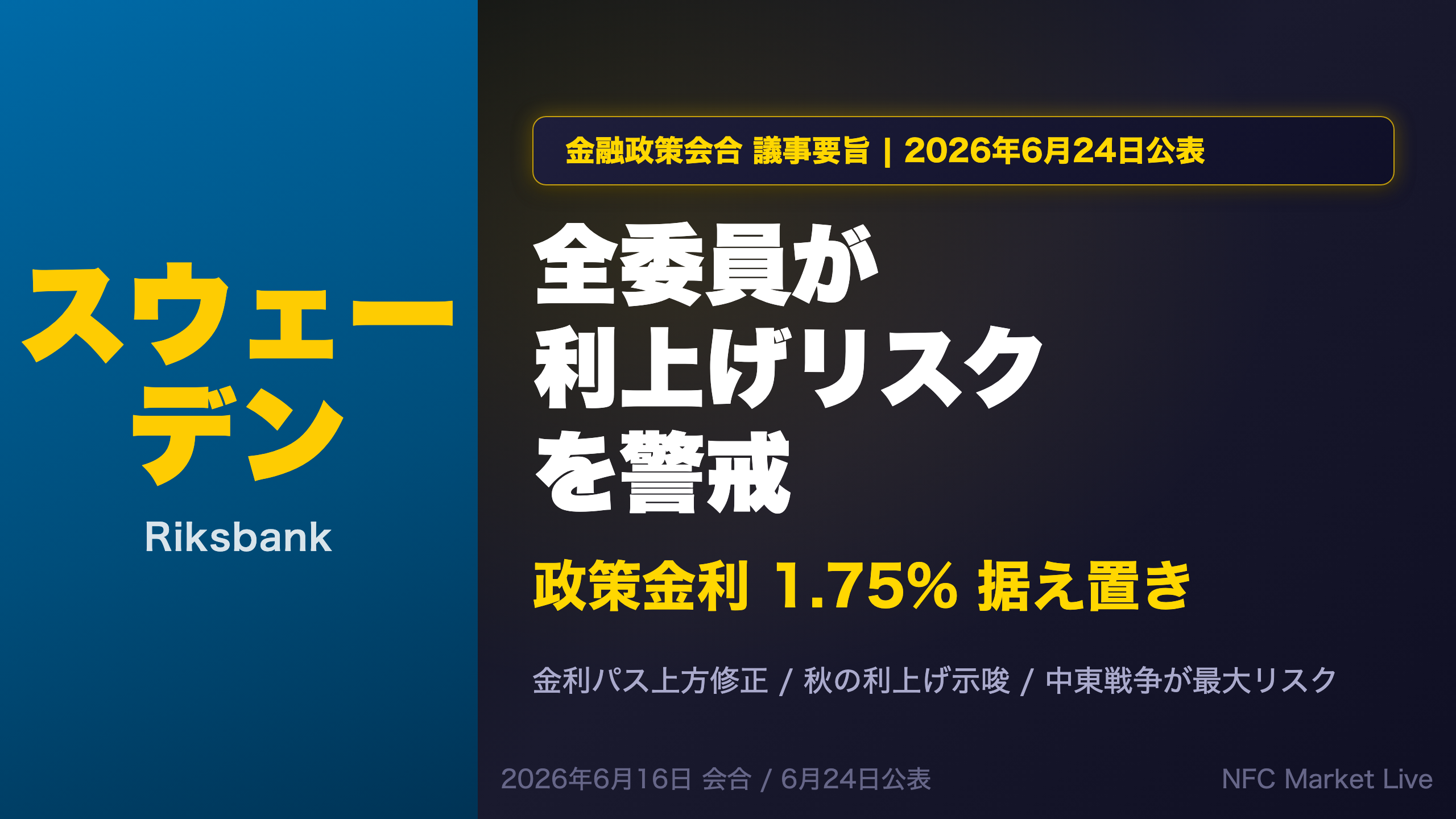

Deep dive into the Riksbank’s June 16, 2026 monetary policy minutes. The policy rate was held unanimously at 1.75%, but all five Executive Board members explicitly flagged upside inflation risks stemming from the Middle East war. The rate path was revised marginally higher vs. March, with a hike to 2.00% now penciled in for late 2027. We break down the hawk-dove dynamics, each member’s key arguments, and what this means for SEK and Swedish rates.

The Ultimate Summary:据え置きの裏に潜む全員一致のタカ派シフト

Executive Summary: Unanimous Hold, But a Quiet Hawkish Pivot

The Riksbank — Sweden’s central bank — published the minutes of its June 16, 2026 monetary policy meeting on June 24. The five-member Executive Board voted unanimously to hold the policy rate at 1.75%, but the minutes reveal a meaningful shift in the board’s collective stance.

Key Decision Metrics

| Item | Detail |

|---|---|

| Policy Rate | 1.75% (held, unanimous) |

| Rate Path | Revised marginally higher vs. March |

| Next Hike Timing | Late 2027 (1.75% → 2.00%, baseline) |

| Change vs. May | Probability of a hike assessed as higher |

Why This Matters

The Riksbank is Sweden’s central bank, equivalent in function to the Federal Reserve or the ECB. It holds eight monetary policy meetings per year. The Executive Board consists of five members: Governor Erik Thedéen, First Deputy Governor Aino Bunge, and Deputy Governors Per Jansson, Anna Seim, and Göran Hjelm.

The defining feature of these minutes is not a hawk-dove split — it is a unanimous directional tilt toward tightening, with differences only in degree and timing. All five members explicitly acknowledged upside inflation risks from the Middle East war, and all supported the marginal upward revision to the rate path.

“Today’s decision means that we are shifting the earlier course in a slightly tighter direction. But the rudder angle remains small — it can be quickly either increased or decreased depending on the evolution of inflationary risks.” — Governor Thedéen

Context: What Changed Since May?

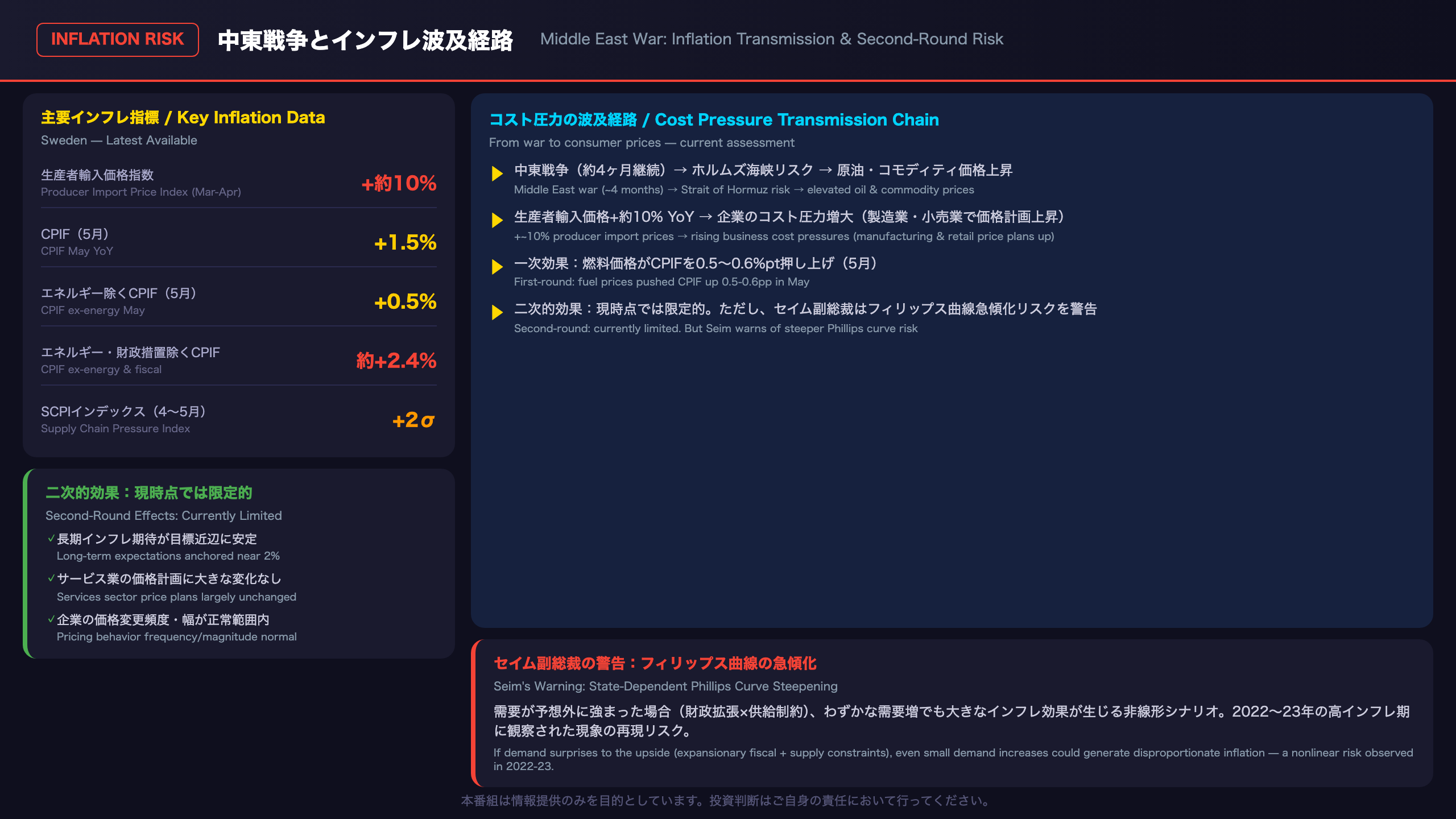

At the May meeting, the board held rates and noted that upside inflation risks had “increased slightly.” By June, four months of elevated oil prices, a roughly 10% year-on-year rise in Sweden’s producer import price index, and rising cost pressures across the business sector had solidified the case for revising the rate path higher. A last-minute U.S.-Iran Memorandum of Understanding (MOU) introduced some uncertainty, but the board judged the situation remained too fragile to materially alter the outlook.

委員別スタンス分析:タカ派スペクトラムの全解剖

Member-by-Member Stance: Full Spectrum Analysis

Hawkish Spectrum (Most → Least)

Thedéen > Seim > Bunge ≈ Hjelm > Jansson

Governor Thedéen (Most Hawkish)

Thedéen delivered the most hawkish statement, warning against “not seeing the wood for the trees” — a metaphor for the risk of missing the broader international inflation picture by focusing too narrowly on domestic indicators. Key points:

- CPIF excluding energy and temporary fiscal measures is already running at ~2.4% — above the 2% target

- US CPI (May) exceeded 4%; euro area inflation rose to just over 3%

- Norges Bank, ECB, and Bank of Japan have already raised rates

- “It is difficult to imagine that Sweden would have a completely different inflation trend than the world around us”

Deputy Governor Jansson (Most Dovish)

Jansson explicitly challenged the concept of “insurance hikes,” arguing:

- Inflation target credibility is currently high — the Riksbank successfully managed both below-target inflation in the 2010s and above-target inflation in 2022-23

- Insurance hikes can only justify “one, or perhaps two, quarter-point increases” — not a meaningful policy tool

- More important: communicate clearly that the bank will act forcefully if inflation becomes a serious problem

- May’s CPIF rise to 1.5% was primarily fuel-driven and should not be interpreted as structural

Deputy Governor Seim (Hawkish-Leaning Middle)

- Even if the Strait of Hormuz reopens, expects a “fragile phase” with continued disruption risk

- Flags the possibility of a steeper Phillips curve (as observed during 2022-23 high inflation), where even small demand increases could generate disproportionate inflation

- Will support a hike when “reliable signs” of worrisome inflation impact emerge

First Deputy Governor Bunge (Centrist)

- Notes that Sweden’s “strikingly low” inflation provides patience to wait

- Highlights the krona’s 2025 appreciation as a key driver of current low inflation — an effect that will fade

- Explicitly signals a “revisit after summer” timeline

Deputy Governor Hjelm (Centrist-Analytical)

- Applies a proprietary analytical framework, assessing the supply shock as “between small and medium-sized”

- Acknowledges the ~10% rise in producer import prices as “alarmingly high” but qualitatively different from the ~40% surge in 2021-22

- Judges second-round effects as currently limited given high inflation target credibility

中東戦争とインフレ:コスト圧力の波及経路と二次的効果リスク

Middle East War Inflation Transmission: Deep Analysis

Transmission Mechanism

The war’s impact on Swedish inflation flows through a clear chain:

- Strait of Hormuz disruption risk → elevated oil, gas, and commodity prices

- Rising import costs → Sweden’s producer import price index up ~10% YoY in March-April

- Business cost pressures → firms’ price plans rising in both the NIER Economic Tendency Survey and the Riksbank’s own Business Survey

- [Bifurcation point] → first-round pass-through to consumer prices (ongoing) vs. second-round effects via wage/price formation behavior (currently limited)

Quantitative Data Summary

| Indicator | Latest | Comparison |

|---|---|---|

| Producer Import Price Index | ~+10% YoY (Mar-Apr) | ~+40% during summer 2021 to mid-2022 |

| Global Supply Chain Pressure Index | ~+2 std dev above avg (Apr-May) | Dec 2021 peak: >+3 std dev |

| Sweden CPIF (May) | +1.5% YoY | Apr: +0.8% |

| CPIF ex-energy (May) | +0.5% YoY | Apr: 0% |

| CPIF ex-energy & fiscal measures | ~+2.4% | Above 2% target |

Why Second-Round Effects Are Currently Limited

All five members agreed second-round effects remain limited, citing:

- Anchored long-term inflation expectations — firmly near the 2% target

- Stable services sector price plans — no change in pricing behavior frequency or magnitude (a key difference from early 2022)

- Normal corporate pricing behavior — firms plan “normal price changes in terms of both magnitude and frequency” (Riksbank Business Survey)

- Collective bargaining framework — social partners expected to use the inflation target as the starting point for upcoming negotiations

Seim’s Warning: State-Dependent Phillips Curve

Deputy Governor Seim introduced the most technically sophisticated risk argument: the possibility that the Phillips curve has steepened (become more state-dependent), as observed during the 2022-23 high inflation episode. In this scenario, even a small increase in economic activity could generate disproportionately large inflation effects. The risk is amplified if expansionary fiscal policy (fuel tax cuts releasing purchasing power) coincides with supply-side constraints from disrupted value chains.

This is a tail risk, not the baseline — but it explains why Seim is more hawkish than Jansson despite both supporting the hold.

金利パスと政策判断の論理:「保険的利上げ」論争の核心

The “Insurance Hike” Debate: Jansson vs. the Majority

Rate Path Changes

| Forecast | Next Hike Timing | Magnitude |

|---|---|---|

| March 2026 | Early 2028 | +0.25% |

| June 2026 | Late 2027 | +0.25% |

| Change | A few quarters earlier | Same |

Jansson’s Case Against Insurance Hikes

Deputy Governor Jansson delivered the most detailed critical analysis of the “insurance hike” concept in these minutes. His argument has four pillars:

-

Credibility prerequisite: Insurance hikes are only justified when there is a credibility problem with the inflation target requiring a clear signal. Sweden does not currently have such a problem.

-

Limited effectiveness: Insurance hikes can only justify “one, or perhaps two, quarter-point increases” — insufficient to fundamentally prevent an inflation surge if one materializes.

-

2022-23 lesson: Jansson argued that the more valid criticism of Riksbank policy in 2022-23 was not that rate hikes started too late, but that the transition to larger increments came too late. The first 50bp hike wasn’t until June 2022; the first 100bp hike wasn’t until late September 2022 — by which point CPIF was already at 9%.

-

Better alternative: Pre-commit to acting “forcefully and decisively” if inflation becomes serious, rather than making small preemptive moves.

The Majority’s “Conditional Preparation” Framework

The other four members — Thedéen, Bunge, Seim, and Hjelm — supported the marginal upward revision to the rate path. Their logic is not “insurance” but “conditional preparation”: maintaining the optionality to hike quickly if Middle East developments warrant it.

“Today’s decision means that we are shifting the earlier course in a slightly tighter direction. But the rudder angle remains small — it can be quickly either increased or decreased depending on the evolution of inflationary risks.” — Governor Thedéen

The U.S.-Iran MOU Factor

News of a U.S.-Iran MOU emerged just days before the meeting but after the June 11 data cut-off date, so it was not incorporated into the forecasts. Jansson explicitly noted that had it been included, it would likely have exerted “marginal downward pressure” on the rate path — a signal that the June rate path revision may already be slightly stale.

インプリケーション:次回会合への示唆と市場への影響

Implications: Next Meeting and Market Impact

Conditions for a Rate Hike at the Next Meeting (Autumn 2026)

Based on the minutes, the five members collectively point to the following triggers for a rate hike:

- Middle East escalation or prolonged disruption: If the MOU fails and the conflict resumes, oil and commodity prices would surge, accelerating cost pass-through

- Accelerating cost pass-through: If producer price increases translate more rapidly into consumer prices than in the baseline

- Change in corporate pricing behavior: If firms begin changing prices more frequently or by larger margins (Seim’s key watchpoint)

- SEK depreciation: An unexpected weakening of the krona would amplify imported inflation (Bunge’s key watchpoint)

- Demand surprise: If fiscal stimulus (fuel tax cuts) releases more purchasing power than expected, interacting with supply constraints

Scenario Matrix

| Scenario | Policy Action |

|---|---|

| Middle East peace + stable inflation | One hike to 2.00% by late 2027 (baseline) |

| Middle East re-escalation + cost acceleration | Multiple hikes in 2026-27 |

| Peace + larger-than-expected indirect effects | Earlier hike, possibly H1 2027 |

Market Implications (Evidence Chain)

Swedish Krona (SEK):

All five members’ hawkish tilt → reduced expectation of rate differential narrowing → modest SEK support. However, Middle East peace progress → risk-off unwinding (SEK positive) vs. lower inflation risk reducing hike probability (SEK negative). These forces may partially offset. It is generally believed that interest rate differentials are a key SEK driver, but the direction cannot be determined from this data alone.

Swedish Government Bonds (SGBs):

Rate path revised higher by a few quarters → upward pressure on short-to-medium maturities. However, Jansson’s skepticism about insurance hikes signals the actual tightening threshold remains high → limited impact on the long end. This is consistent with a modest bear-flattening bias.

Key Watchpoints for the Next Meeting

- Sweden CPIF (June-August): Does the ex-energy, ex-fiscal measure core sustainably exceed 2%?

- Global Supply Chain Pressure Index trajectory

- Middle East: Progress of the MOU and the 60-day negotiation window

- Riksbank Business Survey: Corporate price plans and pricing behavior

- SEK/KIX index: Any unexpected depreciation amplifying imported inflation

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.