📺 Watch the Full Video Analysis

This article was automatically generated by the NFC Market Live AI analysis system. (Updated: 2026-07-09 03:10 JST)

📄 Primary Source

Federal Reserve

https://www.federalreserve.gov/monetarypolicy/fomcminutes20260617.htm

📊 Deep dive into the first FOMC minutes of the Kevin Warsh era (June 16-17 meeting).

⚠️ PCE inflation accelerated to an estimated 4.1% in May, with core PCE at 3.4%.

📈 The 12-0 unanimous hold masks a hawkish pivot: the easing bias was scrubbed from the statement, a few participants saw a case for a rate HIKE, and many judged the appropriate year-end fed funds rate to be ABOVE the current range.

💡 The statement was radically shortened, ending with a blunt pledge: “The Committee will deliver price stability.” Warsh’s five task forces were also recorded in the minutes.

📉 We trace the implications for Treasury yields, the dollar-yen rate, and US equity portfolios. Next meeting: July 28-29.

The Ultimate Summary — 利下げバイアス消滅、ウォーシュFRBのタカ派転換

From 8-4 to 12-0: What the “Unity” Really Means

For readers less familiar with FOMC mechanics: the Federal Open Market Committee sets US interest rates, and its minutes — released three weeks after each meeting — reveal the internal debate behind the decision. These are the first minutes chaired by Kevin Warsh, who succeeded Jerome Powell and famously declared at his debut press conference that “inflation is a choice.”

The April meeting produced a fractured 8-4 vote: Governor Miran dissented in favor of a cut, while Hammack, Kashkari, and Logan objected to keeping an easing bias in the statement. June’s 12-0 unanimity is not a dovish convergence — it is unanimous approval of a statement that deleted the easing bias entirely, meaning the hawks effectively won the argument.

The Inflation Problem

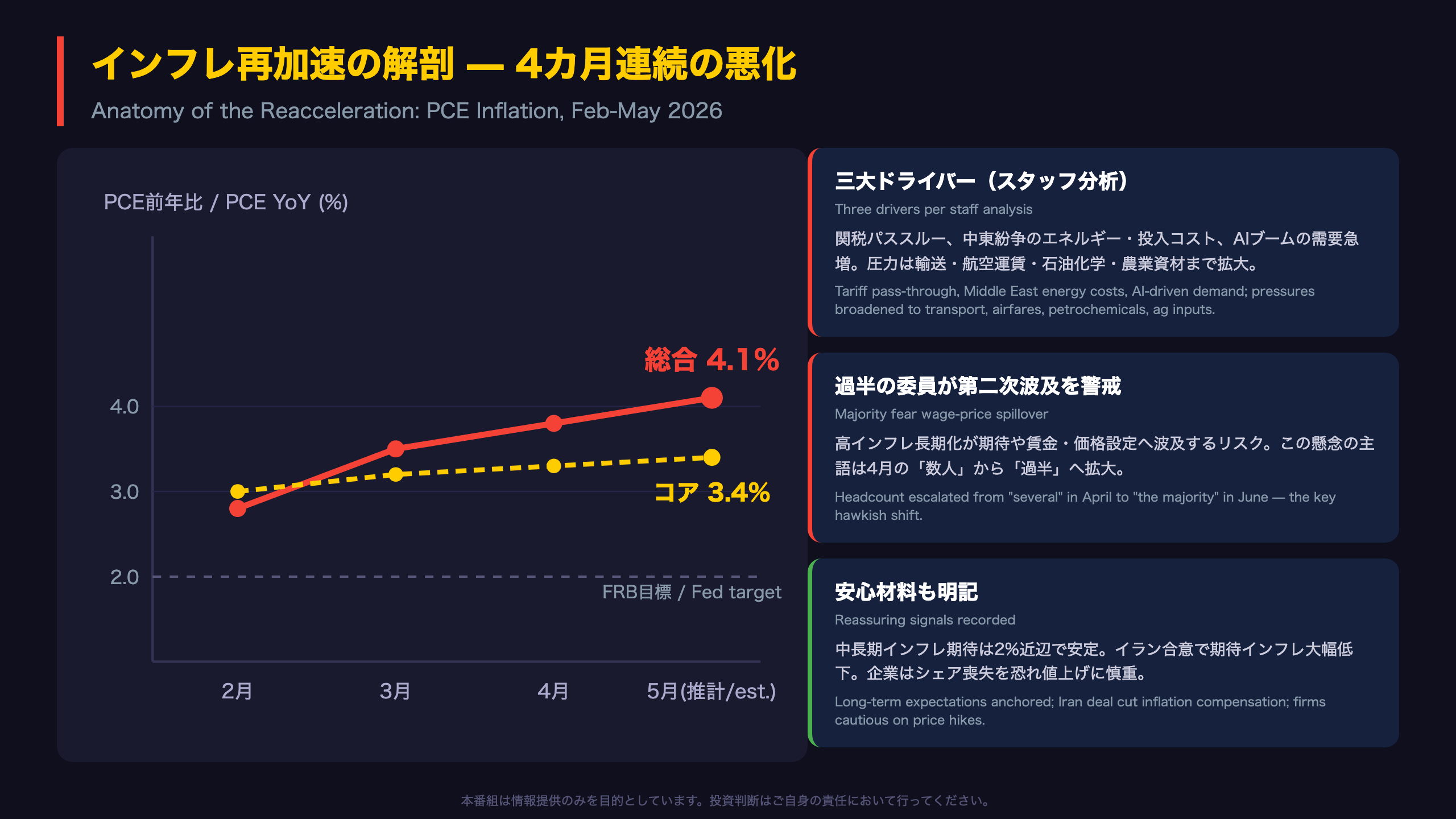

PCE inflation — the Fed’s preferred gauge, broader than CPI — has accelerated four months running: 2.8% in February, 3.5% in March, 3.8% in April, and an estimated 4.1% in May, with core at 3.4%. For comparison, this is more than double the Fed’s 2% target, a starker overshoot than anything the ECB or Bank of England currently faces, and it comes as the ECB has already begun raising rates.

The Decisive Sentence

The new, radically shortened statement ends with a blunt pledge: “The Committee will deliver price stability.” No hedging, no bias language. The minutes also formally record that upside risks to price stability remained elevated while downside employment risks “moderated a bit” — an official tilt of the dual mandate toward the inflation side. Next meeting: July 28-29.

ウォーシュ体制の幕開け — 会議室で何が変わったか

How the Fed’s Boardroom Changed Under Warsh

For context: FOMC statements have followed a highly formulaic template since the financial crisis — long paragraphs covering activity, employment, inflation, risk assessment, and forward guidance, with changes measured word by word. The June statement breaks that mold entirely: just three short paragraphs, no forward guidance, ending with “The Committee will deliver price stability.”

Committee Buy-In, Not a Solo Act

Crucially, the minutes show this was not the chairman acting alone. “A majority of participants remarked that they saw advantages in shortening the statement,” and “most participants” preferred not to repeat the easing-bias language. Some participants “welcomed the opportunity to review the Committee’s communications tools and practices.” In Fed-speak, that is a broad mandate for reform.

The Five Task Forces

The minutes formally record: “The Chairman described plans to establish five independent task forces to examine issues related to the broad conduct of monetary policy.” No design details are given, but the fact that institutional reform entered the official record — rather than remaining press-conference rhetoric — signals it is genuinely in motion.

A Peaceful Transfer of Power

The attendance list now reads “Kevin Warsh, Chairman,” with Jerome Powell listed as a regular governor who voted with the majority. Compare this with leadership transitions at other central banks: an outgoing chief remaining on the board and endorsing his successor’s first statement rewrite is unusual and lends the new regime legitimacy. For investors, the takeaway is that the hawkish pivot carries the full committee’s weight — it will not be easily reversed by internal dissent.

インフレ再加速の解剖 — 4.1%の中身と広がる価格圧力

Anatomy of the Reacceleration: Tariffs, War, and “AI-flation”

Why PCE Matters

For readers used to CPI headlines: the Fed targets PCE inflation, a broader gauge that typically runs a few tenths below CPI. So a 4.1% PCE print is severe — roughly double the 2% target and a larger overshoot than the euro area faced when the ECB began hiking this cycle.

The Three Drivers

Fed staff attributed the acceleration to (1) pass-through of past tariff increases, (2) energy and input costs from the Middle East conflict and the Strait of Hormuz closure, and (3) demand surges from the AI buildout. The third is the novel one: what April’s minutes treated as a niche “IT sector price” issue has been promoted to a core inflation driver. Many participants expected AI infrastructure demand to keep pushing up technology product and electricity prices — a structural, not transitory, force.

Watch the Headcount Language

FOMC minutes encode consensus in carefully graded terms. In April, “several” participants worried inflation could infect wage- and price-setting; in June it became “the majority.” That escalation in the headcount is the single most hawkish sentence-level change in the document.

The Disinflationary Ledger

The minutes are not one-sided: longer-term inflation expectations stayed anchored near 2%, the Iran agreement drove market-based inflation compensation “significantly lower,” housing services disinflation continues, and District business contacts reported caution about raising prices for fear of losing market share. Staff still project inflation returning to about 2% by 2028 — but flagged “emergent price pressures unrelated to tariffs or energy” as a salient persistence risk, for the fifth consecutive set of minutes.

利上げか、維持か — 委員会内の分岐と次の一手の条件

Mapping the Committee’s Split — and the Triggers for the Next Move

How to Read FOMC Headcount Language

The minutes never publish individual votes on the rate path, but their graded vocabulary — “a few,” “several,” “some,” “many,” “most,” “almost all” — functions as a de facto poll. This time it reveals a committee split almost down the middle: “many participants” saw the appropriate year-end rate within or slightly below the current 3.50-3.75% range, while “many other participants” saw it above the range. “A few” argued there was already a case for hiking at this very meeting.

The Neutral-Rate Debate Has Shifted

In April, participants generally judged the policy rate to be “within the range of plausible estimates of its neutral level.” In June, “several” said they did not view policy as restrictive at all. If policy is not restrictive while inflation runs at 4%, the textbook implication is that rates are too low — a quiet but consequential analytical shift that closes the door on near-term cuts.

The Scenario Framework

The minutes lay out an unusually explicit reaction function:

- Firming trigger: inflation stays elevated (AI demand, Middle East, tariffs) against a stable labor market → “almost all” relevant participants saw policy firming as likely warranted.

- Hold/cut trigger: inflationary pressures dissipate and disinflation clearly resumes → hold or eventually cut.

For comparison, market pricing recorded in the minutes implied one hike by mid-2027, while the Desk survey median still showed one cut in Q2 2027 — markets themselves mirror the committee’s split. With downside employment risks judged to have “moderated a bit,” the bar for cuts is now materially higher than in April. The July 28-29 meeting is the next test.

日本人投資家へのインプリケーション — ドル円・米国株・次のアクション

The Chain of Evidence: From the Minutes to Your Portfolio

Dollar-Yen: The Rate-Differential Channel

The minutes explicitly record that the rise in US two-year yields exceeded comparable AFE sovereign yields, and that “consistent with the widening interest rate gap… the U.S. dollar had modestly appreciated.” With the easing bias gone, US short rates should stay elevated — and for yen-based investors, note that the Bank of Japan’s policy rate remains far below the Fed’s 3.50-3.75% range, so the carry argument for the dollar persists. That said, this dataset alone cannot determine the currency path; BOJ policy is the wild card.

US Equities: Earnings vs. Discount Rates

Despite the 10-year Treasury yield rising ~20bp intermeeting (+50bp since the conflict began), the S&P 500 gained nearly 6%, led by technology, with “higher earnings expectations” accounting for most of the move. The lesson: in an AI-driven earnings cycle, higher yields do not mechanically compress equity prices. Caveats recorded in the minutes: elevated valuations raise correction risk if bad news hits, private credit is deteriorating again (BDC inflows slowing, redemptions accelerating), and Treasury ownership is shifting toward price-sensitive private investors — a structural force pushing term premiums higher.

Rates and the Global Backdrop

Unusually, the Fed is now hawkish in sync with peers: the ECB has already hiked in response to energy-driven inflation, and markets price at least one more hike each in the euro area and UK this year. A globally rising-rate environment differs fundamentally from a Fed-alone tightening.

The Checkpoint

July 28-29 is the next meeting. The reaction function is explicit: persistent inflation with stable employment means firming becomes likely; clear disinflation means a hold. Watch core PCE’s path from 3.4% and the jobs reports in between.

Disclaimer: This article is for informational purposes only. All investment decisions are made solely at your own risk.